Alabama A 1 Template

Navigating the obligations of withholding income tax can be daunting for employers, especially when dealing with the specific requirements laid out by state authorities. In Alabama, one crucial tool in this process is the Form A-1, known as the Employer’s Quarterly Return of Income Tax Withheld. This form serves as a declaration by employers of the income tax withheld from their employees' wages during a given quarter. With strict deadlines demanding the form be submitted on or before the last day of the month following the quarter's end, understanding the form's nuances is essential. Employers must note that for payments of $750 or more, electronic filing and payment are mandatory, emphasizing the shift towards digital solutions for tax administration. First-time filers need to secure a withholding tax account number via the state's official tax website, ensuring they are properly registered before tackling Form A-1. The form itself requires detailed information, including the total number of employees, the total Alabama income tax withheld during the period, adjustments for any previous payments or overpayments, and calculation of any penalties or interest due for late filings or payments. This comprehensive structure ensures that all necessary information is meticulously reported, aiding in the streamlined collection and management of withheld income taxes. For employers ceasing to withhold Alabama income tax, the form also facilitates the closing of their withholding account, marking a final submission. With implications for compliance, financial planning, and operational efficiency, the accurate and timely completion of Form A-1 is a critical task for all Alabama employers engaging in the withholding of employee income tax.

Alabama A 1 Example

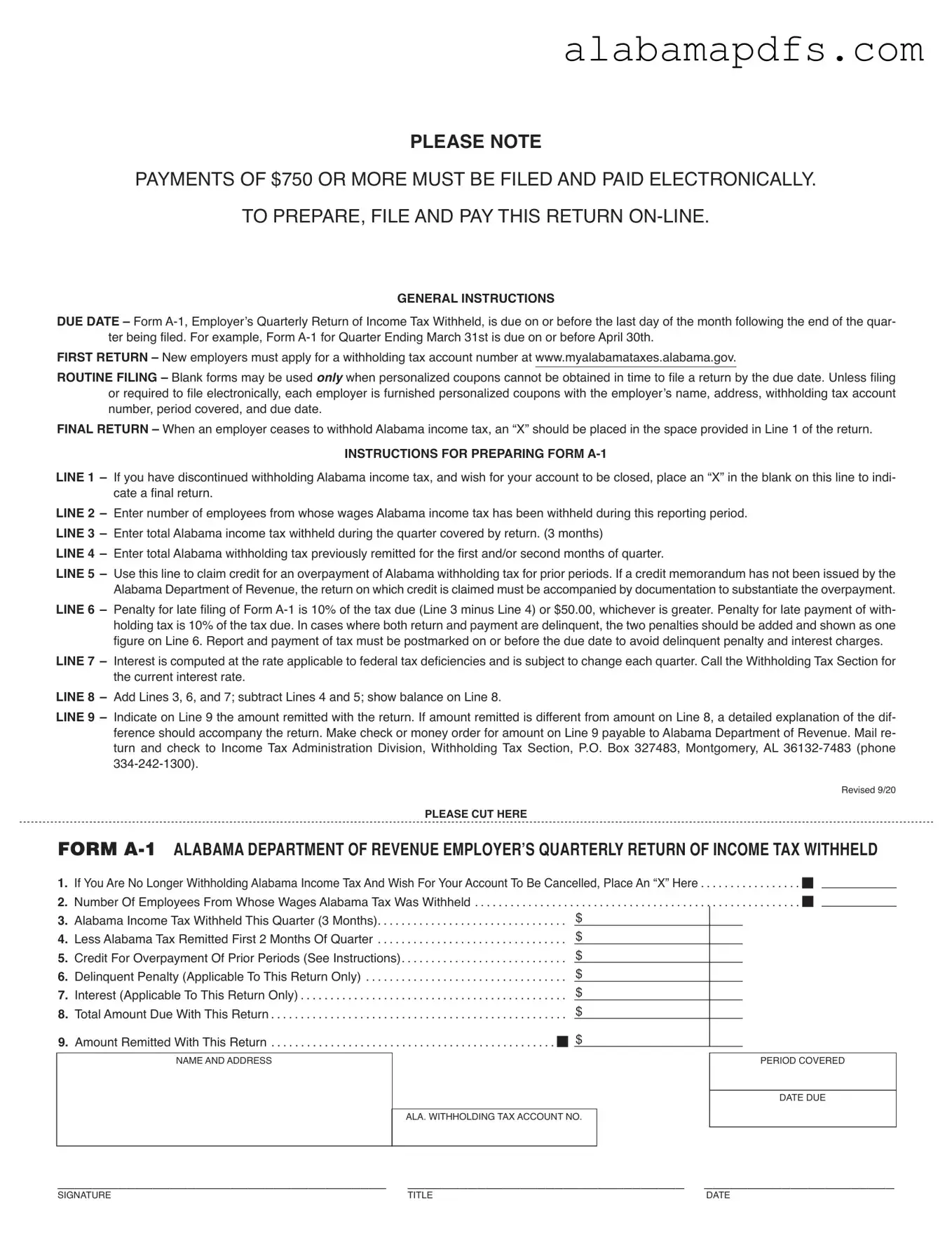

PLEASE NOTE

PAYMENTS OF $750 OR MORE MUST BE FILED AND PAID ELECTRONICALLY.

TO PREPARE, FILE AND PAY THIS RETURN

GENERAL INSTRUCTIONS

DUE DATE – Form

FIRST RETURN – New employers must apply for a withholding tax account number at www.myalabamataxes.alabama.gov.

ROUTINE FILING – Blank forms may be used only when personalized coupons cannot be obtained in time to file a return by the due date. Unless filing or required to file electronically, each employer is furnished personalized coupons with the employer’s name, address, withholding tax account number, period covered, and due date.

FINAL RETURN – When an employer ceases to withhold Alabama income tax, an “X” should be placed in the space provided in Line 1 of the return.

INSTRUCTIONS FOR PREPARING FORM

LINE 1 – If you have discontinued withholding Alabama income tax, and wish for your account to be closed, place an “X” in the blank on this line to indi- cate a final return.

LINE 2 – Enter number of employees from whose wages Alabama income tax has been withheld during this reporting period. LINE 3 – Enter total Alabama income tax withheld during the quarter covered by return. (3 months)

LINE 4 – Enter total Alabama withholding tax previously remitted for the first and/or second months of quarter.

LINE 5 – Use this line to claim credit for an overpayment of Alabama withholding tax for prior periods. If a credit memorandum has not been issued by the Alabama Department of Revenue, the return on which credit is claimed must be accompanied by documentation to substantiate the overpayment.

LINE 6 – Penalty for late filing of Form

LINE 7 – Interest is computed at the rate applicable to federal tax deficiencies and is subject to change each quarter. Call the Withholding Tax Section for the current interest rate.

LINE 8 – Add Lines 3, 6, and 7; subtract Lines 4 and 5; show balance on Line 8.

LINE 9 – Indicate on Line 9 the amount remitted with the return. If amount remitted is different from amount on Line 8, a detailed explanation of the dif- ference should accompany the return. Make check or money order for amount on Line 9 payable to Alabama Department of Revenue. Mail re- turn and check to Income Tax Administration Division, Withholding Tax Section, P.O. Box 327483, Montgomery, AL

Revised 9/20

PLEASE CUT HERE

FORM

1. If You Are No Longer Withholding Alabama Income Tax And Wish For Your Account To Be Cancelled, Place An “X” Here . . . . . . . . . . . . . . . . . y

2. Number Of Employees From Whose Wages Alabama Tax Was Withheld . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . y 3. Alabama Income Tax Withheld This Quarter (3 Months). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

4. Less Alabama Tax Remitted First 2 Months Of Quarter . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

5. Credit For Overpayment Of Prior Periods (See Instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . $

6. Delinquent Penalty (Applicable To This Return Only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

7. Interest (Applicable To This Return Only) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

8. Total Amount Due With This Return . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . $

9. Amount Remitted With This Return . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . y $

NAME AND ADDRESS |

PERIOD COVERED |

DATE DUE

ALA. WITHHOLDING TAX ACCOUNT NO.

______________________________________ ________________________________ ______________________

SIGNATURE |

TITLE |

DATE |

Form Specs

| Fact | Detail |

|---|---|

| Form Title | Alabama A-1 Employer’s Quarterly Return of Income Tax Withheld |

| Electronic Filing Requirement | Payments of $750 or more must be filed and paid electronically. |

| Due Date | Due on or before the last day of the month following the quarter's end. |

| New Employers | New employers must apply for a withholding tax account number at www.myalabamataxes.alabama.gov. |

| Routine Filing | Personalized coupons are provided unless filing electronically or when they cannot be obtained in time. |

| Final Return Indicator | Mark an “X” in Line 1 for final returns when ceasing to withhold Alabama income tax. |

| Penalties | Late filing or payment incurs a penalty of 10% of the tax due or $50.00, whichever is greater. |

| Interest on Late Payment | Interest is calculated at the federal tax deficiency rate and updates quarterly. |

Detailed Guide for Writing Alabama A 1

Filling out the Alabama A-1 Form, an Employer's Quarterly Return of Income Tax Withheld, is a crucial step for employers in the state to comply with tax withholding requirements. This form ensures that income tax withheld from employees' wages is properly reported and remitted to the Alabama Department of Revenue. It's important for employers to be thorough and accurate in completing this form to avoid any penalties or discrepancies. The steps below outline how to fill out the form correctly.

- Before you begin, ensure that you have an Alabama withholding tax account number. If this is your first return and you do not have an account number, register at www.myalabamataxes.alabama.gov.

- At the top portion of the form, if you're no longer withholding Alabama income tax and wish to cancel your account, mark an "X" on Line 1 to indicate a final return.

- Enter the number of employees from whose wages Alabama income tax was withheld during the quarter on Line 2.

- On Line 3, input the total Alabama income tax withheld from all employees during the quarter.

- For Line 4, deduct the total Alabama withholding tax already remitted for the first and/or second months of the quarter.

- If applicable, claim a credit for any overpayment of Alabama withholding tax from prior periods on Line 5. Ensure any claim is accompanied by documentation to substantiate the overpayment unless a credit memo has already been issued by the Alabama Department of Revenue.

- Calculate and note any penalties for late filing on Line 6. Remember, penalties are 10% of the due tax (Line 3 minus Line 4) or $50.00, whichever is greater.

- Interest due for late payment should be computed and entered on Line 7. The interest rate can change each quarter, so it's advised to contact the Withholding Tax Section for the current rate.

- Add Lines 3, 6, and 7, then subtract Lines 4 and 5 to find the total amount due, which you should place on Line 8.

- On Line 9, indicate the total amount remitted with this return. If the amount differs from what is shown on Line 8, attach a detailed explanation for the difference.

- Complete the bottom section with your name, address, the period covered by the return, date due, and your Alabama withholding tax account number. Sign and date the form.

- Make your check or money order payable to the Alabama Department of Revenue and mail the return along with the payment to: Income Tax Administration Division, Withholding Tax Section, P.O. Box 327483, Montgomery, AL 36132-7483. Ensure to contact the provided phone number (334-242-1300) for any further assistance.

After submitting the form and payment as outlined, it's important to keep records of all documentations and confirmations received for your filing. Timely and accurate completion of Form A-1 helps maintain compliance with Alabama's income tax withholding obligations, avoiding potential financial penalties.

Common Questions

What is the Alabama A-1 form used for?

The Alabama A-1 form is an Employer's Quarterly Return of Income Tax Withheld. Employers use this form to report and remit income tax withheld from their employees' wages. It ensures that income tax withholding is accurately reported and paid to the Alabama Department of Revenue on a quarterly basis.

When is the Alabama A-1 form due?

The Alabama A-1 form is due on or before the last day of the month following the end of the quarter being reported. For quarters ending March 31, June 30, September 30, and December 31, the respective due dates are April 30, July 31, October 31, and January 31.

How can new employers apply for a withholding tax account number?

New employers must apply for a withholding tax account number to file the Alabama A-1 form. This can be done online at www.myalabamataxes.alabama.gov. Once registered, employers will receive the necessary information and credentials to file their withholding tax reports.

What should I do if I'm filing my final return?

If you are filing the Alabama A-1 form for the last time because you have ceased withholding Alabama income tax, you should mark an "X" in the space provided on Line 1 of the return. This indicates that it is a final return and that you wish for your withholding tax account to be closed.

How is the penalty for late filing or payment calculated on the Alabama A-1 form?

The penalty for late filing of the Alabama A-1 form is 10% of the tax due or $50.00, whichever is greater. If the withholding tax payment is also late, the same 10% penalty applies to the tax due. Should both the return and the payment be delinquent, both penalties are added together and reported on Line 6 of the form.

Where should the Alabama A-1 form be mailed?

The completed Alabama A-1 form along with the payment should be mailed to: Income Tax Administration Division, Withholding Tax Section, P.O. Box 327483, Montgomery, AL 36132-7483. Employers must ensure that both the report and payment are postmarked by the due date to avoid any penalties and interest charges.

Common mistakes

Filling out tax forms can be a daunting task, especially when the details and instructions are not followed carefully. When completing the Alabama A-1 form, there are common mistakes that many people make. Identifying and avoiding these errors can help ensure the process goes smoothly and accurately.

One of the first missteps is not filing electronically when the payment is $750 or more. The Alabama Department of Revenue requires these payments to be filed and paid online. Ignoring this requirement can lead to processing delays and potential penalties.

Another common error is incorrectly marking Line 1 for final returns. If you have stopped withholding Alabama income tax and need to close your account, you must mark an “X” in the space provided on Line 1. Failing to do so could lead to confusion and unnecessary follow-up by the state to clarify your withholding status.

Mistakes in calculating the total tax withheld during the quarter, which is entered on Line 3, can also be problematic. This total must reflect all Alabama income tax withheld during the three-month period covered by the return. Overlooking or incorrectly adding the amounts withheld can lead to discrepancies and result in under or overpayment of taxes.

- Not filing and paying electronically for payments of $750 or more.

- Incorrectly marking or failing to mark Line 1 for final returns when no longer withholding Alabama income tax.

- Miscalculating the total Alabama income tax withheld during the quarter for Line 3.

Employers also frequently enter incorrect numbers of employees from whose wages Alabama income tax was withheld on Line 2. This figure is crucial for the state to assess the accuracy of the tax withheld relative to the number of employees.

Line 4, which requires the employer to enter the total Alabama withholding tax previously remitted for the first and/or second months of the quarter, is another source of errors. Often, there is failure to accurately report amounts already paid, leading to incorrect tax due calculations.

Finally, misunderstanding penalties and interest calculations on Lines 6 and 7 can significantly affect the total amount due. Penalties for late filing and late payment, along with applicable interest, must be accurately calculated and added to the total tax due to avoid underpayment.

- Entering incorrect employee counts on Line 2.

- Misreporting previously remitted taxes on Line 4.

- Miscalculating penalties and interest on Lines 6 and 7.

To avoid these common mistakes, it is crucial to read the instructions carefully, double-check calculations, and ensure that all required documentation is accurate and complete. This will help in timely and accurate filing of the Alabama A-1 form, minimizing the risk of errors and potential penalties.

Documents used along the form

Filing tax documents often involves a tapestry of forms, each serving its unique purpose in the financial and regulatory landscape. For employers in Alabama managing withholding taxes, the A-1 form marks just the beginning. Several other forms and documents are commonly used in conjunction with the Form A-1 to ensure a thorough and compliant approach to tax filing. Understanding these associated documents can streamline the process, ensuring that all bases are covered.

- Form A-3: This annual reconciliation form is a must for employers, aimed at reconciling the total income tax withheld from employees throughout the year with the quarterly submissions made using Form A-1. It's a way of double-checking that what was supposed to be withheld matches what was actually withheld and submitted.

- Form W-2: Essential for nearly every employer, the W-2 form reports an employee's annual wages and the amount of taxes withheld from their paycheck. It's a critical piece of the puzzle, providing documentation that supports the quarterly and annual filings made to the state.

- Form 1099: For businesses that work with freelancers, contractors, or any non-employee service providers, Form 1099 is used to report the income paid to these individuals. It's an important document for ensuring that all income is accounted for, not just that paid to traditional employees.

- Form A-4: Employees use this form to determine the amount of state income tax to be withheld from their paychecks. It's a crucial document for employers to collect and maintain, as it affects the calculations for the quarterly A-1 form filings.

- Business Privilege Tax Return: Though not directly linked to employee withholding, this return is essential for most Alabama businesses, calculating a tax based on the entity’s ability to conduct business within the state. It’s a cornerstone of a company’s tax obligations and complements the withholding reporting requirements.

Grappling with these forms might seem daunting, but together, they create a comprehensive framework for managing a business's tax responsibilities. Each plays a role in ensuring the accurate reporting of income and taxes, safeguarding businesses against potential discrepancies and legal issues. As intricate as this network of documents can be, understanding their purposes and interconnections simplifies the task of tax filing, allowing employers to maintain focus on their business's growth and success.

Similar forms

The Alabama A-1 form, designated for employers to report quarterly income tax withheld from employees, bears similarities with other tax documents in structure and objective. Remarkably, its counterparts can be found at both federal and state levels, guiding the withholding and reporting of income tax.

Form 941, Employer's Quarterly Federal Tax Return, serves as a prime example. Like the Alabama A-1, Form 941 is a quarterly submission required by the IRS to report income taxes, Social Security tax, or Medicare tax withheld from employees’ paychecks. Additionally, it captures the employer's portion of Social Security or Medicare tax. The similarity lies in their quarterly filing requirement, focus on withholding taxes, and the need to reconcile taxes withheld with the amounts actually remitted to the tax authorities. Both forms serve as a means for the government to monitor and collect taxes pertinent to employee earnings within a given quarter.

Another analogous document is the State Unemployment Tax Act (SUTA) return. Although the primary function of SUTA is for unemployment tax reporting to state agencies, it parallels the Alabama A-1 form in frequency, being a quarterly obligation for most employers. The SUTA return contributes to state unemployment benefits pools, directly tying to employee wages much like the Alabama A-1’s role in withholding income tax. The distinction mainly lies in the type of tax collected and reported; however, both documents are crucial for compliance with respective state and federal tax laws.

The Alabama A-1 form also shares features with the W-2 form, Wage and Tax Statement. While the W-2 is an annual report provided to employees, detailing wages paid and taxes withheld during the year, it complements the data reported quarterly through the Alabama A-1. Employers use information from the A-1 forms to accurately complete W-2 forms. Here, the connection is not in the document’s recipients or the frequency of submission but in the flow of information. The A-1 forms aggregate the quarterly data that ultimately gets reported annually on the W-2, ensuring employees receive accurate year-end summaries for income tax purposes.

Dos and Don'ts

When filling out the Alabama A-1 form, it’s important to follow some key guidelines to ensure the process is smooth and error-free. Here are things you should do and things you shouldn't do:

Should Do:- File electronically if your payment is $750 or more, as this is a requirement.

- Apply for a withholding tax account number at www.myalabamataxes.alabama.gov if this is your first return.

- Make sure your return is submitted on time—by the last day of the month following the quarter’s end.

- Place an “X” in the designated space if you are filing a final return because you have ceased to withhold Alabama income tax.

- Accurately enter the number of employees from whose wages Alabama income tax has been withheld.

- Forget to calculate penalties and interest correctly if your return or payment is late. Penalties are 10% of the tax due or $50, whichever is greater, plus interest on late payments.

- Ignore overpayments: Claim credit for any overpayment of Alabama withholding tax for prior periods but ensure documentation is provided to substantiate the claim.

- Mail your return without ensuring that the accompanying check or money order is made payable to the Alabama Department of Revenue and sent to the correct address.

Following these guidelines helps avoid potential mistakes that could lead to penalties or a delay in processing your return.

Misconceptions

Understanding the complexities of state tax forms is critical for employers, especially those in Alabama grappling with the A-1 form, a cornerstone in reporting withheld income tax. However, misconceptions abound, leading to confusion and mistakes that can be costly in terms of both time and penalties. Here are five common misunderstandings related to the Alabama A-1 form, demystified for clarity.

Electronic Filing is Optional for Payments Under $750: There's a common belief that if the total payment is less than $750, employers can opt out of electronic filing. This is not entirely accurate. While the form explicitly mandates electronic filings for payments of $750 or more, it implicitly encourages digital submissions for all transactions to streamline processing and reduce errors.

New Employers Do Not Require Immediate Registration: Another prevalent misconception is that new businesses have a grace period before needing to register for a withholding tax account. In reality, obtaining a withholding tax account number from the Alabama Department of Revenue's My Alabama Taxes website is one of the first steps a new employer must take before filing their first return.

Personalized Coupons Are Mandatory for Filing: Some employers believe they cannot file their return without personalized coupons, which are furnished with details like the employer's name, address, and withholding tax account number. While these coupons ease the filing process, the form's instructions clarify that blank forms may be used if personalized coupons are not available by the due date, debunking the notion of their absolute necessity.

Final Return Indicators Are Optional: The assumption that marking a return as final is optional when an employer ceases to withhold Alabama income tax is incorrect. To correctly notify the Alabama Department of Revenue of the cessation of business or payroll activities, an "X" must be placed in the specified space on Line 1 of the form, making it a required action rather than optional.

Overpayment Credits Require Official Memos Only: There's a misunderstanding that claiming a credit for overpayment of Alabama withholding tax for previous periods strictly requires an official credit memorandum issued by the Alabama Department of Revenue. While having such a memo simplifies the process, employers can substantiate their claim with documentation if a memo has not been issued, as stated in the instructions for Line 5.

Clarifying these misconceptions helps ensure that employers fulfill their tax obligations correctly, avoiding the pitfalls of penalties and interest for misunderstandings. As always, when in doubt, consulting directly with the Department of Revenue or a tax professional can provide guidance tailored to specific circumstances.

Key takeaways

Filling out and using the Alabama A-1 form, the Employer’s Quarterly Return of Income Tax Withheld, is an essential task for employers in Alabama. Here are some key takeaways to consider:

- Electronic Filing Requirement: If the payment is $750 or more, the form must be filed and paid electronically. This helps streamline the process and ensures timely submission.

- Due Date: The form is due the last day of the month following the quarter’s end. For instance, the due date for the first quarter (ending March 31) is April 30.

- Registration for New Employers: New employers must apply for a withholding tax account number online at www.myalabamataxes.alabama.gov before filing their first return.

- Use of Blank Forms: Personalized coupons are typically provided for routine filing. However, blank forms may be used if personalized coupons are not available before the filing deadline.

- Final Return: Marking an "X" in the space provided on Line 1 indicates a final return, used when an employer stops withholding Alabama income tax.

- Calculating Penalties: Late filings incur a penalty of 10% of the due tax or $50, whichever is greater. Similar penalties apply for late payments, and interest is charged on due amounts.

- Making Payments: Payments should be made to the Alabama Department of Revenue, with checks or money orders payable as described on the form. Correct submission addresses and payment details are crucial to avoid processing delays.

Understanding and adhering to these points ensures proper compliance with Alabama's tax withholding requirements, avoiding penalties, and ensuring efficient processing of employer tax duties.

Check out Popular PDFs

Alabama 3 - It must be filed even if there are no state tax withholdings in a given period to maintain compliance with Alabama tax laws.

Alabama Ppt - Privilege Tax Due must be paid by the original due date of the return without regard for filing extensions.

Medicaid Renewal Application Online - Falsifying information or omitting crucial details can lead to denial and possible legal action.