Alabama 2100 Template

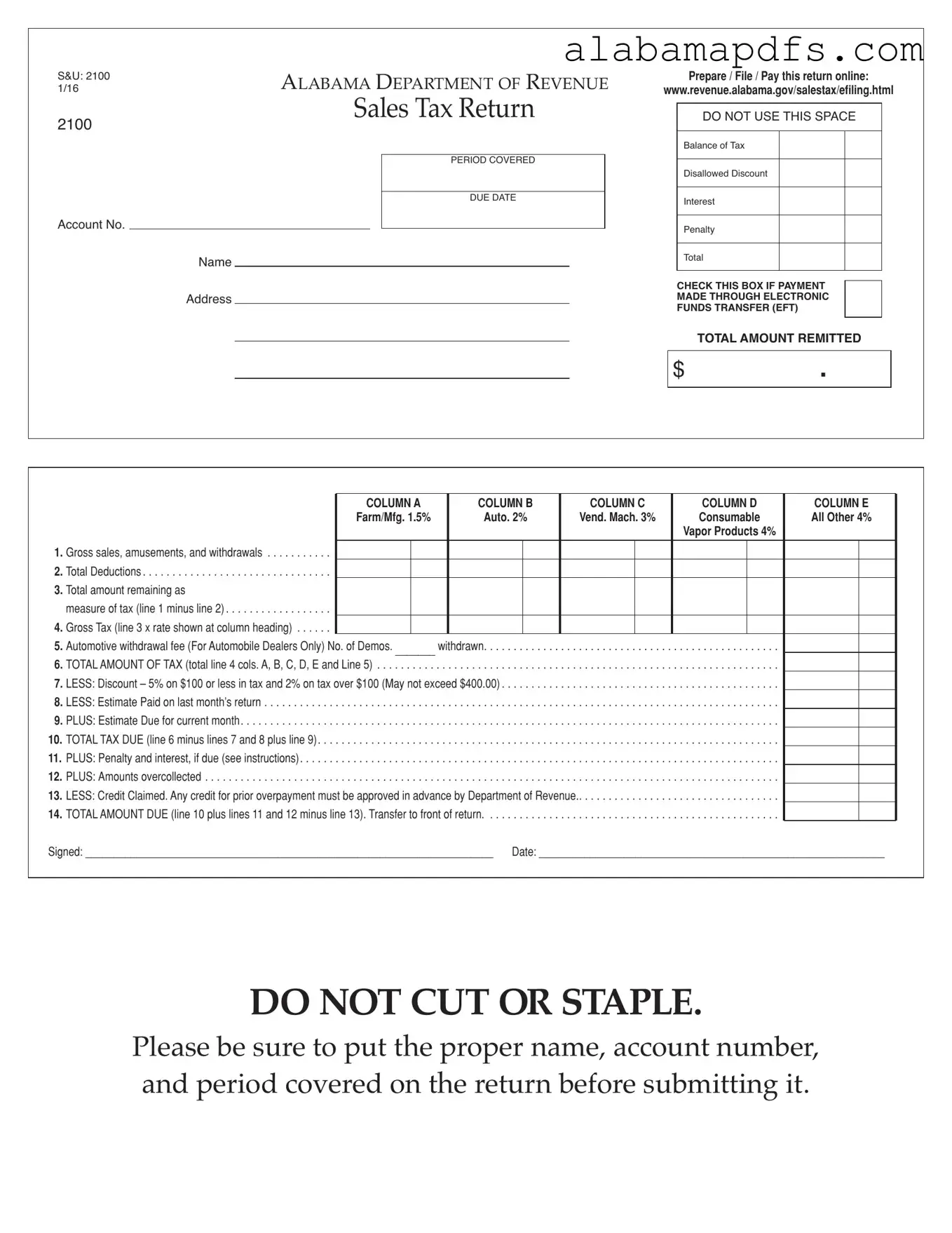

The Alabama 2100 form is a crucial document for businesses operating within the state, mandating the accurate reporting and payment of sales taxes to the Alabama Department of Revenue. Crafted to ensure compliance and facilitate the efficient collection of taxes, this form requires detailed information about sales, categorized by different tax rates such as Farm/Mfg. at 1.5%, Auto at 2%, Vend. Mach. at 3%, Consumable and All Other at 4%, and Vapor Products at 4%. Businesses must report gross sales, amusements, withdrawals, and total deductions to calculate the total amount of tax due. Additionally, the form encompasses sections for automotive withdrawal fees specifically for automobile dealers, discounts for timely payments, adjustments for estimated payments from previous months, and penalties and interest if applicable. Moreover, it includes a provision for claiming credits for overpayments, subject to prior approval by the Department of Revenue, enhancing the form's role in promoting fairness and accuracy in tax reporting and payment. Reminders are provided to ensure the correct information is included before submission, and the option for electronic fund transfers (EFT) signals the department's move towards modernizing tax payments, underscoring the broad scope and meticulous detail captured in the Alabama 2100 form, all designed to streamline the sales tax remittance process.

Alabama 2100 Example

S&U: 2100 |

AlAbAmA DepArtment of revenue |

|

|

|

Prepare / File / Pay this return online: |

||||||||||||||||||||||

1/16 |

|

|

www.revenue.alabama.gov/salestax/efiling.html |

||||||||||||||||||||||||

|

|

|

|

Sales tax return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

2100 |

|

|

|

|

|

|

|

|

DO NOT USE THIS SPACE |

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Balance of Tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PERIOD COVERED |

|

|

|

|

|

|

Disallowed Discount |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

DUE DATE |

|

|

|

|

|

|

Interest |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Account No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Penalty |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CHECKTHISBOXIFPAYMENT |

|

|

|

|

|

||||

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MADETHROUGHELECTRONIC |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FUNDSTRANSFER(EFT) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

TOTALAMOUNTREMITTED |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

. |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

COLUMN A |

COLUMN B |

|

COLUMN C |

|

|

|

COLUMN D |

|

COLUMN E |

|

||||||||||||

|

|

|

|

|

Farm/Mfg. 1.5% |

Auto. 2% |

|

Vend. Mach. 3% |

|

|

|

Consumable |

|

All Other 4% |

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Vapor Products 4% |

|

|

|

|

|

|

|

||

1. |

. .Gross sales, amusements, and withdrawals |

. . . . . . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

2. |

. . . . . . . . . . . . . . . . . . . . . . .Total Deductions |

. . . . . . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

3. |

Total amount remaining as |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

measure of tax (line 1 minus line 2) |

. . . . . . . . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

4. |

. . . . . .Gross Tax (line 3 x rate shown at column heading) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

5. |

Automotive withdrawal fee (For Automobile Dealers Only) No. of Demos. _______ withdrawn |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

6. |

TOTAL AMOUNT OF TAX (total line 4 cols. A, B, C, D, E and Line 5) |

. . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

||||||||

7. |

. . . . . . . . . . . . . . . . . . . . . . .LESS: Discount – 5% on $100 or less in tax and 2% on tax over $100 (May not exceed $400.00) |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

||||||||||||

8. |

. . .LESS: Estimate Paid on last month’s return |

. . . . . . . . . |

. . . . . . |

. . |

. . . . . |

. . . . . . |

. . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

|||

9. |

. . . . . . .PLUS: Estimate Due for current month |

. . . . . . . . . |

. . . . . . |

. . |

. . . . . |

. . . . . . |

. . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

|||

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .10. TOTAL TAX DUE (line 6 minus lines 7 and 8 plus line 9) |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

||||||||||

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .11. PLUS: Penalty and interest, if due (see instructions) |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

||||||||||

. . . . . . . . . . . . . . . . . . . . . .12. PLUS: Amounts overcollected |

. . . . . . |

. . |

. . . . . |

. . . . . . |

. . . . . . . . . . . . . |

. . . . . . |

. . . . . . . . |

. . . . . |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

|||||

13. LESS: Credit Claimed. Any credit for prior overpayment must be approved in advance by Department of Revenue |

|

|

|

|

|

|

|

||||||||||||||||||||

. . . . . . . . . . . . . . . . . . . . . . . . . .14. TOTAL AMOUNT DUE (line 10 plus lines 11 and 12 minus line 13). Transfer to front of return |

. . . . |

. |

. |

. |

. . . . . . . . . . . . |

. . . . . |

|

|

|

|

|

|

|

|

|||||||||||||

Signed: ________________________________________________________________________ |

Date: _____________________________________________________________ |

DO NOT CUT OR STAPLE.

please be sure to put the proper name, account number, and period covered on the return before submitting it.

Form Specs

| Fact | Description |

|---|---|

| Form Type | Alabama Sales Tax Return Form 2100 |

| Filing Options | Can be prepared, filed, and paid online through the Alabama Department of Revenue's e-filing system. |

| Tax Rates | Includes varied sales tax rates for different categories: Farm/Mfg. (1.5%), Auto (2%), Vend. Mach. (3%), Consumable and All Other (4%), and Vapor Products (4%). |

| Discount Application | Allows for a discount on taxes paid: 5% on $100 or less in tax and 2% on amounts over $100, with a maximum discount of $400.00. |

| Governing Law | Regulated under the State of Alabama's tax codes and governed by the Alabama Department of Revenue. |

Detailed Guide for Writing Alabama 2100

Filling out the Alabama 2100 form for sales tax can seem daunting at first, but it's a straightforward process when broken down step by step. This crucial document ensures that your business stays compliant with the state's tax obligations. Before you start, make sure you have all relevant sales data and financial records at hand. This will make the process smoother and help avoid errors. Below are the steps you need to follow to accurately complete the Alabama 2100 form.

- Visit the Alabama Department of Revenue website to access the form online: www.revenue.alabama.gov/salestax/efiling.html. You have the option to prepare, file, and pay for this return online.

- Fill in the "Account No." field with your unique sales tax account number.

- Enter your business’s Name and Address in the designated sections.

- Indicate the PERIOD COVERED by this return, ensuring you have the correct beginning and ending dates.

- Specify the DUE DATE according to the tax reporting schedule your business follows.

- Check the box if PAYMENT IS MADE THROUGH ELECTRONIC FUND TRANSFER (EFT).

- In the COLUMN A - COLUMN E section, enter the applicable gross sales, deductions, and calculate the tax for each tax rate category:

- Enter gross sales, amusements, and withdrawals in the appropriate column based on the tax rate (COLUMN A for Farm/Mfg. 1.5%, COLUMN B for Auto. 2%, etc.).

- Input total deductions and subtract this from your gross sales to find the total amount remaining as the measure of tax for each column.

- Calculate the gross tax by multiplying the total amount remaining by the tax rate shown at each column heading.

- For automobile dealers, fill in the "Automotive withdrawal fee", including the number of demonstrations withdrawn.

- Sum up the TOTAL AMOUNT OF TAX, taking into account all columns and the automotive withdrawal fee.

- Apply the appropriate LESS: Discount based on your tax amount. Remember, the discount is 5% on $100 or less in tax and 2% on tax over $100, not to exceed $400.

- Subtract any Estimate Paid on last month’s return, and add any Estimate Due for the current month.

- Calculate the TOTAL TAX DUE by subtracting the discount (and any estimate paid last month) from the total amount of tax, then add the estimate due for the current month.

- Add any Penalty and interest, if due, along with any Amounts overcollected.

- Subtract any Credit Claimed that has been approved in advance by the Department of Revenue.

- The TOTAL AMOUNT DUE is the final amount you owe. Transfer this figure to the front of the return.

- Ensure the form is signed and dated before submission.

- Double-check all entries for accuracy, and make sure you've put the proper name, account number, and period covered on the return before submitting it.

Remember, accuracy is key when it comes to tax documents. Double-checking your calculations and ensuring all information is up-to-date can save you time and headaches later. If you have any questions or need clarification, the Alabama Department of Revenue is always a good resource. Taking it step by step can make the process of filling out the Alabama 2100 form less intimidating and help keep your business in good standing.

Common Questions

What is the Alabama 2100 form used for?

The Alabama 2100 form is a sales tax return document that businesses use to report and pay the sales tax owed to the Alabama Department of Revenue. It covers various rates for different categories such as general sales, automotive, vending machines, consumables, and vapor products. Businesses must fill out this form to accurately report their gross sales, calculate the appropriate taxes due, and claim any eligible discounts or credits.

How can one file the Alabama 2100 form?

Businesses can prepare, file, and pay for the Alabama 2100 form online via the Alabama Department of Revenue’s website dedicated to sales tax e-filing. The website provides a streamlined process for submitting the form and making payments, ensuring accuracy and timeliness in fulfilling state tax obligations.

What is the due date for submitting the Alabama 2100 form?

The due date for submitting the Alabama 2100 form and any associated payment varies depending on the taxation period and the filing schedule assigned to your business by the Alabama Department of Revenue. Generally, the due date is specified on the form for the period covered. It's essential to submit the form and complete payment by the indicated due date to avoid penalties and interest charges.

Can discounts be claimed on the Alabama 2100 form?

Yes, discounts can be claimed on the Alabama 2100 form. A business is eligible for a 5% discount on the first $100 of tax due and a 2% discount on any tax amount over $100. However, the total discount cannot exceed $400.00. This discount is intended to compensate for the costs of collecting and remitting state sales taxes.

What should be done if an electronic funds transfer (EFT) is used?

If you make a payment through electronic funds transfer (EFT), you should check the box on the Alabama 2100 form indicating that payment was made through EFT. This notifies the Department of Revenue that payment will be processed electronically, which is separate from the submission of the sales tax return form.

How are gross sales reported on the Alabama 2100 form?

Gross sales, along with amusements and withdrawals, should be reported in the designated sections on the Alabama 2100 form. The form includes columns for different types of transactions and rates, ensuring the appropriate calculation of taxes based on the nature of the sales. Proper reporting of gross sales is crucial for calculating the correct amount of tax due.

What happens if tax is overcollected?

In cases where tax is overcollected, the amount should be added to the total tax due on the Alabama 2100 form. It is important to accurately report overcollected taxes to ensure compliance with state laws and regulations. Overcollected taxes are treated as due to the state and must be remitted accordingly.

Is there a penalty for late submission or payment?

Yes, there is a penalty for late submission or payment of the Alabama 2100 form. Penalties and interest may apply if the form is not filed and the payment is not made by the due date specified for the covered period. It's essential to adhere to the submission deadlines to avoid additional charges.

How is a credit claimed for a prior overpayment?

To claim a credit for a prior overpayment on the Alabama 2100 form, the credit must first be approved in advance by the Department of Revenue. Once approved, the amount can be deducted in the designated section of the form. This ensures that businesses only claim legitimate credits, and it helps streamline the adjustment process.

Common mistakes

Filling out the Alabama 2100 form, a crucial process for reporting sales tax, often involves several common errors. These mistakes can delay processing and potentially lead to penalties. Becoming aware of these errors can help ensure that your submissions are accurate and timely.

- Incorrect Account Numbers: One of the first mistakes made is entering an incorrect account number. This critical piece of information links your tax return to your business, so double-check for accuracy before submitting.

- Disregarding the Pre-filled Areas: Sometimes, the form comes with certain areas pre-filled based on previous submissions or estimates. Disregarding these can lead to inconsistencies in reporting and under- or overpayment of taxes.

- Miscalculating Deductions: Rather than diligently subtracting total deductions from gross sales, some rush through this calculation. This haste can result in an inaccurate tax base and subsequent incorrect tax amounts.

- Misapplying Tax Rates: Each column on the form corresponds to different tax rates for various categories of goods. Applying the wrong tax rate to gross sales is a recurring issue, especially when dealing with multiple rate categories.

- Overlooking the Automotive Withdrawal Fee: For automobile dealers, there's a specific section on the form devoted to the automotive withdrawal fee. Failure to account for this can lead to an understated tax liability.

- Incorrect Discount Applications: The form allows for a discount under specific conditions, but this section is often erroneously filled. It's essential to understand the eligibility criteria for discounts to avoid this mistake.

- Failure to Account for Electronic Fund Transfers (EFT): If you're making payments through EFT, there's a designated checkbox that many overlook. Neglecting to check this box when applicable can cause confusion regarding payment methods.

- Leaving Signature and Date Areas Blank: Completing the return is not just about the numbers; it's also a legal document that requires a signature and date. Forgetting to sign or date the form can render it invalid.

To ensure a smooth submission process, individuals must be diligent, double-check their calculations, and thoroughly review the form before submission. Paying close attention to the common mistakes listed can considerably reduce the risk of errors and the additional work required to correct them.

Remember, accurate and timely submissions not only comply with state tax laws but also prevent unnecessary penalties and interest. Should doubts or questions arise, seeking clarification from the Alabama Department of Revenue or a tax professional is advisable.

Documents used along the form

The Alabama 2100 form, pivotal for reporting and paying sales tax, is a fundamental document within the state's tax administration framework. Supplementing this key form, a variety of other forms and documents are often utilized to ensure comprehensive compliance and accurate financial reporting. These complementary items play crucial roles in clarifying, detailing, and substantiating the entries recorded on the Alabama 2100 form, thereby facilitating a smoother interaction with tax regulations.

- Schedule of Collections (Form BPT-V): This form serves as a detailed record of the sales tax collected by the business, broken down by tax rate and jurisdiction. It provides the necessary details to support the gross sales and collections reported.

- Business Privilege Tax Return (Form PPT or CPT): Filed annually, this document reports the amount of business privilege tax due, based on the business’s net worth and applicable rate for its business type. It often accompanies sales tax forms to report and pay different types of taxes.

- Alabama Department of Revenue Power of Attorney (Form 2848A): This form authorizes an individual, such as an accountant or attorney, to communicate with the revenue department and make decisions on behalf of the filer regarding tax matters.

- Application for Sales Tax Certificate of Exemption (Form STE-1): Businesses purchasing goods for resale can use this form to apply for a sales tax exemption certificate, allowing them to buy goods without paying sales tax at the point of purchase.

- Consumer Use Tax Return (Form CPT or PPT): When businesses purchase goods or services without paying Alabama sales tax, this form allows them to report and pay the required use tax on those purchases.

- Sales Tax Exemption Certificate for Governmental Entities (Form ST-EXC-3): This certificate allows qualifying governmental entities to purchase goods and services without paying sales tax, which must be filed alongside the standard sales tax forms when making exempt purchases.

- Local Sales Tax Return Forms: In addition to state sales tax, businesses may need to file local sales tax returns for the specific municipalities or counties where they operate, requiring separate forms provided by local revenue departments.

- Annual Recap of Federal Income Tax Return (Form AR): This form summarizes key financial data from the business’s federal income tax return, providing a snapshot that may be necessary for reconciling sales and income tax liabilities.

- Estimated Tax Payment Vouchers (Form 40ES): Used by individuals or entities to make quarterly estimated tax payments when the expected tax due on income, including profit from sales, is not covered by withholdings.

In conclusion, navigating the complexities of Alabama's tax obligations involves more than just the Alabama 2100 form. The additional forms and documents listed above are integral to providing a comprehensive and detailed account of a business's financial and tax situation. Whether it's providing detailed sales collections, applying for tax exemptions, or authorizing a power of attorney, these accompanying documents ensure that businesses can meet their tax responsibilities fully and accurately.

Similar forms

The Alabama 2100 form, primarily used for sales tax returns, shares similarities with a variety of other tax documents designed for both specific and general purposes. An important aspect to note is how these documents, while tailored for different tax facets, maintain a fundamental structure aimed at ensuring tax compliance and accurate reporting. Let's delve into some of these documents and identify the commonalities and unique features that link them to the Alabama 2100 form.

Form 1099 is a federal document used to report income other than wages, salaries, and tips. Like the Alabama 2100 form, the 1099 is comprehensive in its approach to capturing income-related transactions. Both forms are pivotal during the tax season, ensuring individuals and businesses correctly report earnings and pay any taxes due. The key similarity lies in their role in tax administration: ensuring the correct tax amounts are remitted based on reported figures. However, the 2100 form is more focused on sales transactions for businesses within Alabama, while Form 1099 encompasses a wider variety of income across the entire United States.

The Uniform Commercial Code (UCC) Filing is another document that, at first glance, might not seem directly related to the Alabama 2100 form, yet shares foundational commonalities. The UCC filing, used to declare a security interest in a transaction, ensures that lenders have a claim to collateral if a borrower defaults. Similar to the 2100 form’s objective of tax reporting for sales transactions, the UCC filing plays a crucial role in the financial documentation of transactions. Both forms serve to legally document specific types of transactions, providing a structured way to declare, for tax or lending purposes, how money is being exchanged or what liabilities exist.

State-Specific Sales Tax Forms, such as New York’s ST-100, California’s BOE-401-EZ, and Texas’s Form 01-114, are quite similar to the Alabama 2100 form in function and purpose. These forms are tailored to each state’s specifications for reporting and paying sales tax, mirroring the Alabama 2100’s role within Alabama. Each form requires detailed reporting of sales revenues, applicable tax rates, and deductions or exemptions, ensuring that businesses comply with state tax laws. What differentiates them is the state-specific information, tax rates, and categories unique to the local economy and tax legislation, while their underlying purpose of facilitating state tax collection remains the same.

Dos and Don'ts

Filling out official forms can seem like a chore, but with the right approach, it can be a smooth and mistake-free process. The Alabama 2100 form, a staple for reporting sales tax, is no exception. To ensure accuracy and compliance, here are some essential dos and don'ts to keep in mind:

- Do ensure you have the correct form for the reporting period. The Alabama Department of Revenue updates forms, and using an outdated version can lead to processing delays.

- Do double-check your calculations. Errors in math can result in underpayment or overpayment of taxes, both of which can be problematic.

- Do report all applicable sales accurately. Underreporting sales can result in penalties and interest.

- Do take advantage of the discount for timely filing, if applicable, but ensure it does not exceed the maximum allowed.

- Do verify your account number and the period covered before submission. These details are crucial for your return to be processed correctly.

- Don't staple or cut the form. This can cause issues with the processing of your document.

- Don't leave sections blank. If a section does not apply, it's better to enter "N/A" or "0" to indicate it's been acknowledged but isn't applicable.

- Don't forget to include your payment if you're not making an electronic funds transfer (EFT). Doing so can result in a delay in the processing of your return.

- Don't send your return without signing and dating it. An unsigned return is considered incomplete and will not be processed.

Following these guidelines can help ensure that your Alabama 2100 form is filled out correctly and processed without delay. Remember, when in doubt, referring to the instructions provided by the Alabama Department of Revenue or seeking professional advice can be very helpful.

Misconceptions

Understanding the Alabama 2100 form is critical for accurate and timely sales tax filing. However, several misconceptions can lead to errors. Addressing these misconceptions ensures compliance and avoids unnecessary penalties.

- Misconception 1: The Alabama 2100 form can only be filed on paper.

Contrary to this belief, the Alabama 2100 form can, and is encouraged to be, filed online. This process not only saves time but also reduces the likelihood of errors.

- Misconception 2: Discounts are automatically calculated.

Discounts are not automatically calculated by the system. Filers must calculate and apply the appropriate discount, ensuring it does not exceed $400.00.

- Misconception 3: All sales are taxed at the same rate.

The form outlines different tax rates for different types of sales, including Farm/Mfg. at 1.5%, Auto at 2%, Vend. Mach. at 3%, and others at 4%. It is crucial to apply the correct tax rate to the corresponding sales type.

- Misconception 4: The due date is the same each month.

Due dates may vary, and it is the responsibility of the business to be aware of the current month’s due date to avoid penalties for late submissions.

- Misconception 5: Automotive withdrawal fee applies to all businesses.

This fee is specific to automobile dealers only, related to the number of demos withdrawn. Other businesses do not need to calculate this fee.

- Misconception 6: Electronic Funds Transfer (EFT) is optional for all.

For businesses that meet certain criteria, EFT payments are mandatory. Checking the EFT box indicates compliance with this requirement.

- Misconception 7: Overpayments are automatically refunded.

Refunds for overpayments must be requested, and any credit for prior overpayment must be approved in advance by the Department of Revenue.

- Misconception 8: The total amount remitted equals total sales.

The total amount remitted is the result of various calculations, including gross sales, deductions, tax rates application, discounts, and penalties. It is not simply the total of gross sales.

Understanding and addressing these misconceptions is crucial for accurate and compliant sales tax reporting. The Alabama Department of Revenue encourages thorough review of instructions and utilizing their available resources to ensure the Alabama 2100 form is correctly completed and submitted.

Key takeaways

Filling out the Alabama 2100 form correctly is crucial for accurately reporting and paying sales tax. These key takeaways ensure that individuals and businesses handle the process efficiently and in compliance with state requirements.

- Preparation is key: Before starting, gather all necessary sales records and information to accurately report gross sales, deductions, and the net tax amount.

- Identify the correct tax rates: The form requires different tax rates for various categories such as Farm/Mfg. at 1.5%, Auto at 2%, Vend. Mach. at 3%, Consumable and All Other at 4%, and Vapor Products at 4%. Ensure you apply the correct rate to your sales.

- Online filing option: Alabama encourages online filing, which can be done through the Department of Revenue's website. This facilitates a quicker and more efficient submission process.

- Complete all sections accurately: Every section of the form must be filled out to reflect your sales activities. Inaccuracies can lead to penalties or an audit.

- Understand deductions: Properly account for all allowable deductions to avoid overpayment of taxes. Ensure that the deductions are well documented in case of any future inquiries from the Department of Revenue.

- Calculate discounts correctly: There’s a discount for timely filing and payment – 5% on $100 or less in tax and 2% on tax over $100, not to exceed $400.00. Ensure this is calculated accurately to take advantage of the savings.

- Electronic Funds Transfer (EFT): Check the EFT box if you are making the payment electronically. This is an efficient way to submit payment directly from a bank account.

- Penalties and interest: Late filings or payments can result in penalties and interest charges. It’s crucial to submit both the form and payment by the due date to avoid additional costs.

- Keep records: After submitting the form, keep a copy for your records along with all relevant sales documentation. This is important for future reference and for validating the information submitted on the form.

Awareness and adherence to these key points when completing and submitting the Alabama 2100 form can help ensure compliance with sales tax regulations, avoid penalties, and make the process smoother and more efficient.

Check out Popular PDFs

Alabama W2 - The integration of electronic filing for Form A-3 and attached W-2s by eligible Alabama employers marks a step towards streamlined, eco-friendly tax administration practices.

Sbi Alabama - It links each incident to a unique case number, ensuring easy retrieval and reference.