Alabama 20S Template

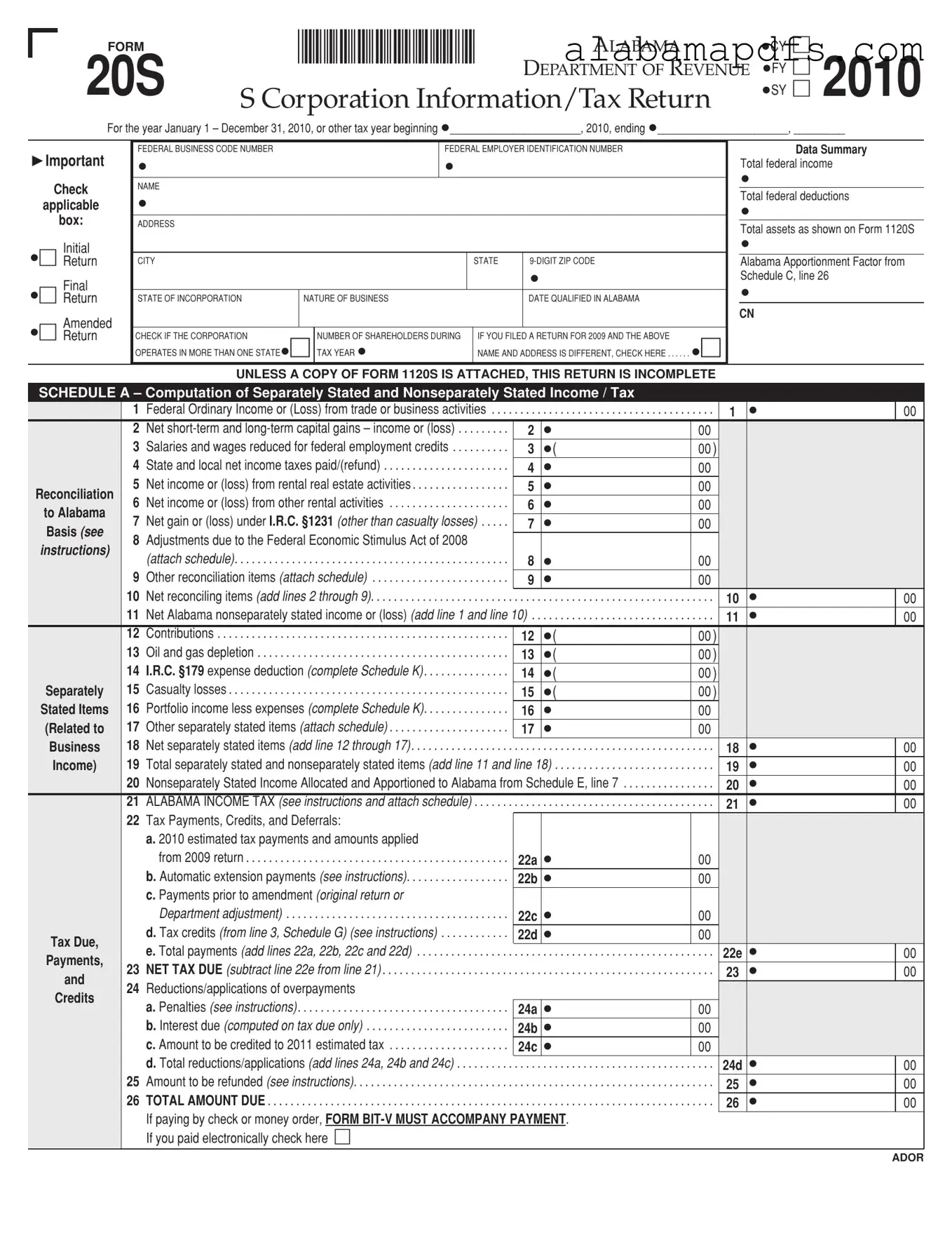

The Alabama 20S form, officially known as the S Corporation Information/Tax Return, serves as a critical document for S corporations operating within the state of Alabama. This form, tailored for the tax year 2010, mandates comprehensive disclosure of financial activities ranging from January 1 to December 31, 2010, or for any other fiscal period beginning in 2010. It requires detailing the S corporation's total federal income, deductions, and assets as reported on Form 1120S, alongside the Alabama Apportionment Factor from Schedule C, line 26. The form encompasses various schedules, including Schedule A for income/tax computation, Schedule B for allocation of nonbusiness income, and Schedule C for apportionment factor calculation, among others. S corporations must accurately report their state of incorporation, nature of business, and operational details, including whether they operate across state lines. Crucially, failure to attach a copy of the Form 1120S renders the return incomplete, emphasizing the interconnectedness of federal and state tax obligations. Schedule K, integral to the return, details the distributive share items, highlighting the importance of accurately apportioning income and deductions among shareholders. Additionally, tax credits, payments, and potential overpayments are meticulously addressed, underscoring the form's comprehensive scope in facilitating S corporations' adherence to Alabama's tax regulations.

Alabama 20S Example

FORM |

*1000012S* |

ALABAMA |

•CY |

|

|

|

20S |

|

|

|

|

|

|

|

DEPARTMENT OF REVENUE |

•SY |

2010 |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

•FY |

|

|

|||||||

|

|

|

|

|

S Corporation Information/Tax Return |

|

|

|

|

||||||||||||

|

For the year January 1 – December 31, 2010, or other tax year beginning •_______________________, 2010, ending •_______________________, _________ |

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Important |

|

FEDERAL BUSINESS CODE NUMBER |

|

|

FEDERAL EMPLOYER IDENTIFICATION NUMBER |

|

|

|

|

|

|

Data Summary |

||||||||

|

|

• |

|

|

|

• |

|

|

|

|

|

|

|

Total federal income |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Check |

|

NAME |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total federal deductions |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

applicable |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

||||

|

box: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

ADDRESS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total assets as shown on Form 1120S |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

Initial |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

• |

Return |

|

CITY |

|

|

|

|

|

STATE |

|

|

|

|

Alabama Apportionment Factor from |

|||||||

|

Final |

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

Schedule C, line 26 |

||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

||

Return |

|

STATE OF INCORPORATION |

NATURE OF BUSINESS |

|

|

DATE QUALIFIED IN ALABAMA |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

CN |

|

|

|

|||||||||||

|

Amended |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Return |

|

CHECK IF THE CORPORATION |

|

NUMBER OF SHAREHOLDERS DURING |

IF YOU FILED A RETURN FOR 2009 AND THE ABOVE |

|

|

|

|

|

|

|

|

||||||||

|

|

|

OPERATES IN MORE THAN ONE STATE• |

|

TAX YEAR • |

NAME AND ADDRESS IS DIFFERENT, CHECK HERE |

• |

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

UNLESS A COPY OF FORM 1120S IS ATTACHED, THIS RETURN IS INCOMPLETE |

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

SCHEDULE A – Computation of Separately Stated and Nonseparately Stated Income / Tax |

|

|

|

|

|

|

|

|

|||||||||||||

|

|

1 |

Federal Ordinary Income or (Loss) from trade or business activities . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

1 |

|

• |

|

|

00 |

||||||||

|

|

2 |

Net |

2 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

3 |

. . . . . . . . . .Salaries and wages reduced for federal employment credits |

3 |

•( |

00 ) |

|

|

|

|

|

|

|

||||||||

|

|

4 |

. . . . . . . . . . . . . . . . . . . . . .State and local net income taxes paid/(refund) |

4 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

5 |

Net income or (loss) from rental real estate activities |

|

|

|

|

|

|

|

|

|

|

|

|||||||

Reconciliation |

5 |

• |

00 |

|

|

|

|

|

|

|

|||||||||||

6 |

Net income or (loss) from other rental activities |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

to Alabama |

6 |

• |

00 |

|

|

|

|

|

|

|

||||||||||

|

7 |

Net gain or (loss) under I.R.C. §1231 (other than casualty losses) |

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

7 |

• |

00 |

|

|

|

|

|

|

|

|||||||||||

|

Basis (SEE |

|

|

|

|

|

|

|

|||||||||||||

|

8 |

Adjustments due to the Federal Economic Stimulus Act of 2008 |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

INSTRUCTIONS) |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

(attach schedule) |

|

|

|

|

|

|

8 |

• |

00 |

|

|

|

|

|

|

|

||

|

|

|

|

. . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

|

|

|

|

|

|

|

|||||

|

|

9 |

. . . . . . . . . . . . . . . . . . . . . . . .Other reconciliation items (attach schedule) |

9 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

10 |

Net reconciling items (add lines 2 through 9) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

10 |

|

• |

|

|

00 |

|||||||||

|

|

11 |

. .Net Alabama nonseparately stated income or (loss) (add line 1 and line 10) |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

11 |

|

• |

|

|

00 |

||||||||||

|

|

12 |

Contributions . . . |

. . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

12 |

•( |

00 ) |

|

|

|

|

|

|

|

||

|

|

13 |

. . . . . . . .Oil and gas depletion |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

13 |

•( |

00 ) |

|

|

|

|

|

|

|

|||

|

|

14 |

. . . . . . . . . . . . . . .I.R.C. §179 expense deduction (complete Schedule K) |

14 |

•( |

00 ) |

|

|

|

|

|

|

|

||||||||

|

|

15 |

Casualty losses . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Separately |

. . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

15 |

•( |

00 ) |

|

|

|

|

|

|

|

||||

|

Stated Items |

16 |

. . . . . . . . . . . . . . .Portfolio income less expenses (complete Schedule K) |

16 |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

(Related to |

17 |

Other separately stated items (attach schedule) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

17 |

• |

00 |

|

|

|

|

|

|

|

|||||||||||

|

|

18 |

Net separately stated items (add line 12 through 17) |

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Business |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

18 |

|

• |

|

|

00 |

|||||||||

|

Income) |

19 |

. . . . . . . . . . . . . . . . . . . . . . . .Total separately stated and nonseparately stated items (add line 11 and line 18) |

. . . . |

19 |

|

• |

|

|

00 |

|||||||||||

|

|

20 |

. . . . . . . . . . . .Nonseparately Stated Income Allocated and Apportioned to Alabama from Schedule E, line 7 |

. . . . |

20 |

|

• |

|

|

00 |

|||||||||||

|

|

21 |

ALABAMA INCOME TAX (see instructions and attach schedule) |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

21 |

|

• |

|

|

00 |

|||||||

|

|

22 |

Tax Payments, Credits, and Deferrals: |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

a. 2010 estimated tax payments and amounts applied |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

from 2009 return |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

22a |

• |

00 |

|

|

|

|

|

|

|

||

|

|

|

|

. . . . . . . . . . . . . . . . . .b. Automatic extension payments (see instructions) |

22b |

• |

00 |

|

|

|

|

|

|

|

|||||||

|

|

|

|

c. Payments prior to amendment (original return or |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

Department adjustment) . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

22c |

• |

00 |

|

|

|

|

|

|

|

||

|

Tax Due, |

|

|

. . . . . . . . . . . .d. Tax credits (from line 3, Schedule G) (see instructions) |

22d |

• |

00 |

|

|

|

|

|

|

|

|||||||

|

Payments, |

|

|

. . . . . . . . . .e. Total payments (add lines 22a, 22b, 22c and 22d) |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

22e |

• |

|

|

00 |

|||||||

|

23 |

NET TAX DUE (subtract line 22e from line 21) |

|

|

|

|

|

23 |

|

• |

|

|

00 |

||||||||

|

and |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

|

|

|

||||||||||||

|

24 |

Reductions/applications of overpayments |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

Credits |

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

a. Penalties (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . |

24a |

• |

00 |

|

|

|

|

|

|

|

|||

|

|

|

|

. . . . . . . . . . . . . . . . . . . . . . . . .b. Interest due (computed on tax due only) |

24b |

• |

00 |

|

|

|

|

|

|

|

|||||||

|

|

|

|

c. Amount to be credited to 2011 estimated tax |

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

24c |

• |

00 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

d. Total reductions/applications (add lines 24a, 24b and 24c) |

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

24d |

• |

|

|

00 |

||||||||

|

|

25 |

. . . . . . . . . . . . . . . . . . . . .Amount to be refunded (see instructions) |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

25 |

|

• |

|

|

00 |

|||||||

|

|

26 |

. . . . . .TOTAL AMOUNT DUE |

. . . |

. . . . . . . . . . . . . . . . . . . . . |

. . . . . |

. |

. . . . . . . |

. . |

. . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . |

26 |

|

• |

|

|

00 |

|||

|

|

|

|

If paying by check or money order, FORM |

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

If you paid electronically check here |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ADOR |

|

|

*1000022S* |

Page 2 |

|

FORM 20S – 2010 |

|

|

|

|

SCHEDULE B – Allocation of Nonbusiness Income, Loss, and Expense |

|

|

|

|

|

Identify by account name and amount all items of nonbusiness income, loss, and expense removed from apportionable income and those items which are directly allocable to Alabama. Adjustment(s) must also be made for any proration of expenses under Alabama Income Tax Rule

allowable deduction that is applicable to both business and nonbusiness income of the taxpayer shall be prorated to each class of income in determining income subject to tax as provided…” (See instructions).

|

DIRECTLY ALLOCABLE ITEMS |

|

ALLOCABLE GROSS INCOME / LOSS |

|

|

|

RELATED EXPENSE |

|

NET OF RELATED EXPENSE |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

Column A |

|

Column B |

|

|

Column C |

|

Column D |

|

Column E |

|

Column F |

|||

|

|

|

Everywhere |

|

Alabama |

|

|

Everywhere |

|

Alabama |

|

Everywhere |

|

Alabama |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Col. A less Col. C) |

(Col. B less Col. D) |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Nonseparately stated items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1a |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1b |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1c |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1d Total (add lines 1a, 1b, and 1c) |

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

• |

||

Separately stated items |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1e |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1f |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1g |

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1h Total (add lines 1e, 1f, and 1g) |

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

• |

||

SCHEDULE C – Apportionment Factor Schedule. Do not complete if entity operates exclusively in Alabama. |

|

|

|||||||||||||||

|

TANGIBLE PROPERTY AT COST FOR |

|

|

ALABAMA |

|

|

|

|

|

EVERYWHERE |

|||||||

|

PRODUCTION OF BUSINESS INCOME |

BEGINNING OF YEAR |

|

END OF YEAR |

|

BEGINNING OF YEAR |

|

END OF YEAR |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Inventories |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

Land |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Furniture and fixtures |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Machinery and equipment |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

Buildings and leasehold improvements |

• |

|

|

|

|

|

|

|

|

|

|

|

|

|||

6 |

IDB/IRB property (at cost) |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Government property (at FMV) |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

Less Construction in progress (if included) |

• |

|

|

|

|

|

|

|

|

|

|

|

|

|||

10 |

Totals |

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

11 |

Average owned property (BOY + EOY ÷ 2) |

|

|

|

• |

|

|

|

|

|

|

|

• |

|

|||

12 |

Annual rental expense |

|

|

• |

x8 = |

• |

|

|

|

• |

|

x8 = |

• |

|

|||

13 |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . .Total average property (add line 11 and line 12) |

|

13a |

• |

|

|

|

. . . . . . |

. . . . |

. . . . . . . . . . . . |

13b |

• |

|

||||

14 |

Alabama property factor — 13a ÷ 13b = line 14 |

. |

. . . . . . |

. . . . . . |

. . . . . . . . . . . |

. . . . . . . |

. . . . . |

. . . . . . . |

. . . . |

. . . . . . . . . . . . |

14 |

• |

% |

||||

|

SALARIES, WAGES, COMMISSIONS AND OTHER COMPENSATION |

|

|

15a |

ALABAMA |

|

15b |

EVERYWHERE |

15c |

|

|||||||

|

RELATED TO THE PRODUCTION OF BUSINESS INCOME |

|

|

|

|

|

|

|

|

|

|

|

|

||||

15 |

Alabama payroll factor — 15a ÷ 15b = 15c |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

% |

|||

|

|

|

SALES |

|

|

|

|

ALABAMA |

|

|

EVERYWHERE |

|

|

||||

16 |

Destination sales |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

17 |

. . . . . . . . . . . . . . . . . . . . . . . .Origin sales |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

18 |

. . . . .Total gross receipts from sales |

. . . . . . . . . . . . . . . . |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|

19 |

. . . . . . . . . . . . . . . . . . . . . . . .Dividends |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

20 |

. . . . . . . . . . . . . . . . . . . . . . . .Interest |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

21 |

. . . . . . . . . . . . . . . . . . . . . . . .Rents |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

22 |

. . . . . . . . . . . . . . . . . . . . . . . .Royalties |

. . |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

||

23 |

. . . . . . .Gross proceeds from capital and ordinary gains |

. . . . . . . . . . . . . . . . . . . . . . |

. . |

. . . . |

• |

|

|

|

|

|

|

|

|

|

|||

24Other •___________________________________ (Federal 1120S, line •_____ ) •

25 |

Alabama sales factor — 25a ÷ 25b = line 25c |

25a• |

25b• |

|

25c• |

% |

26 |

Sum of lines 14, 15c, and 25c ÷ 3 = ALABAMA APPORTIONMENT FACTOR (Enter here and on line 4, Schedule E, page 3) |

26 |

• |

% |

||

ADOR

*1000032S* |

|

|

FORM 20S – 2010 |

|

Page 3 |

SCHEDULE D – Apportionment of Federal Income Tax |

|

|

1 Enter the federal income tax from Federal Form 1120S |

1 • |

00 |

2Enter the Alabama income from line 7, Schedule E below, if applicable. (If corporation operates

|

exclusively in Alabama, do not complete lines |

|

. . . . . |

. |

. . . . . . . . . . . . . |

. . . . 2 |

• |

00 |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Apportionment of separately stated items |

|

|

|

|

|

|

|

|

x • |

% = 3c |

|

|

|

|

|

||

3 |

|

3a |

|

• |

|

|

3b |

|

• |

00 |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter in line 3a the amount from line 18, Schedule A |

|

|

|

|

Apportionment Factor |

|

|

|

|

|

|

||||||

|

|

|

|

|

(line 26, Schedule C) |

|

|

|

|

|

||||||||

4 |

Separately stated items allocated to Alabama (line 1h, Column F, Schedule B) |

. . . . 4 |

• |

00 |

|

|

|

|||||||||||

5 |

Total (add lines 2, 3c and 4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . . . . |

. |

. . . . . . . . . . . . . |

. . . . 5 |

• |

00 |

|

|

|

||||||

6 |

. . . . . . . . . . . . . . .Adjusted total income (add line 19, Schedule A to line 1h, Column E, Schedule B) |

. . . . 6 |

• |

00 |

|

|

|

|||||||||||

7 |

Federal income tax apportionment factor |

(line 5 divided by line 6) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 7 |

• |

% |

|||||||||

8 |

Federal income tax apportioned to Alabama (multiply line 1 by the percent on line 7) |

|

|

|

|

|

|

|

|

|

||||||||

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 8 |

• |

00 |

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

SCHEDULE E – Apportionment and Allocation of Income to Alabama |

|

|

|

|

|

|

|

% |

||||||||||

1 |

Net Alabama nonseparately stated income or (loss) from line 11, Schedule A |

. |

. . . . . |

. |

. . . . . . . . . . . . . . . |

. . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . 1 |

• |

00 |

|||||||

2 |

Nonseparately stated (income) or loss treated as nonbusiness income (line 1d, Column E, Schedule B) |

|

|

|

|

|

||||||||||||

|

|

|

|

|

||||||||||||||

|

– please enter income as a negative amount and losses as a positive amount |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . 2 |

• |

00 |

||||||||||||

3 |

Apportionable income or (loss) (add line 1 and line 2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

. . . . . . . . . . . |

. |

. . . . . |

. |

. . . . . . . . . . . . . . . |

. . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . 3 |

• |

00 |

||||||||

4 |

Apportionment ratio from line 26, Schedule C |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

. . . . . . . . . . . . . . . . |

. . . . . . . . . . . |

. |

. . . . . |

. |

. . . . . . . . . . . . . . . |

. . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . 4 |

• |

% |

|||||||

5 |

Income or (loss) apportioned to Alabama (multiply amount on line 3 by percent on line 4) |

|

|

|

|

|

|

|

|

|||||||||

. . . . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . . . |

. . . . 5 |

• |

00 |

|||||||||||||

6 |

Nonseparately stated income or (loss) allocated to Alabama as nonbusiness income (Column F, line 1d, Schedule B) |

|

|

|

|

|||||||||||||

. . . . 6 |

• |

00 |

||||||||||||||||

7 |

Nonseparately Stated Income Allocated and Apportioned to Alabama (add lines 5 and 6). Also enter this amount on |

|

|

|

|

|||||||||||||

|

line 2, Schedule D; line 20, Schedule A; and line 1, Schedule K |

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 7 |

• |

00 |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

SCHEDULE F – Alabama Accumulated Adjustments Account |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

1 |

Beginning balance (prior year ending balance) . . . |

. . . . . . . . . . . . . . . . . . . . . . . . |

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 1 |

• |

00 |

||||||

2 |

Net Alabama nonseparately stated income or (loss) (line 11, Schedule A) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 2 |

• |

00 |

|||||||||

3 |

Net separately stated items (line 18, Schedule A) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

. . . . . . . . . . . . . . . . . . . . . . . . |

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 3 |

• |

00 |

|||||||

4 |

Federal income tax deduction (line 1, Schedule D) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 4 |

• |

00 |

|||||||||

5 |

Separately stated nonbusiness items (line 1h, Column E, Schedule B) |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 5 |

• |

00 |

|||||||||

6 |

Other additions/(reductions) (Do not include tax exempt income and related expenses) |

|

|

|

|

|

|

|

|

|||||||||

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 6 |

• |

00 |

|||||||||||||

7 |

Less distributions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . |

. . . . . |

|

. . . . . . . . . . . . . . . . . . . . . . . . |

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 7 |

• |

00 |

|||||

8 |

Ending balance (total appropriate lines) . . |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . |

. . . . . |

|

. . . . . . . . . . . . . . . . . . . . . . . . |

. |

. . . . . |

|

. . . . . . . . . . . . . . |

. . . . |

. . . . . . |

. . . . . . . . . . . . . . . . . . . . |

. . . 8 |

• |

00 |

|||||

SCHEDULE G – Tax Credits (CAUTION – SEE INSTRUCTIONS) |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

1 |

Employer Education Tax Credit |

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . . . . . |

|

. . . . . . . . . . . . . . . . . . . . . . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

1 |

• |

00 |

||||||

2 |

Coal Credit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. . . |

. . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . |

|

. . . . . . |

|

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

2 |

• |

00 |

|||||||

3 |

. . . . . . . . . .TOTAL (add lines 1 and 2). Enter here and on line 22d, Schedule A |

. . . . . . |

|

. . . . . . . . . . . . . . . . . . . . |

. . . . . . . |

. . . . . . . . . . . . . . . . . . . . . . . . . . |

3 |

• |

00 |

|||||||||

SCHEDULE H – The Following Information Must Be Entered For This Return To Be Considered Complete |

|

|

||||||||||||||||

1 |

Indicate tax accounting method used: |

• |

|

Cash • |

Accrual |

• |

Other |

|

|

|

|

|

|

|

|

|||

2Briefly describe your Alabama operations: •

3Enter this company’s Alabama Withholding Tax Account No.: •

4Person to contact for information concerning this return:

Name •

Telephone Number • ( |

) |

Email Address |

|

|

|

|

|

5Location of the corporate records: •

6Check if an Alabama business privilege tax return was filed for this entity: •

7If the privilege tax return was filed using a different FEIN, please provide the name and FEIN used to file the return:

FEIN: • |

NAME: |

|

|

|

|

ADOR

*1000042S*

FORM 20S – 2010

SCHEDULE K – Distributive Share Items

1 Alabama Nonseparately Stated Income (Schedule E, line 7) . . . . . .

Separately Stated Items:

2 Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

3 Oil and gas depletion . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

4 I.R.C. §179 expense deduction

a. Amount allowed on federal Form 1120S . . . . . . . . . . . . . . . . . . . . .

b. Adjustments required . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

c. Amount to be apportioned . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5 Casualty losses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6 Portfolio income. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7 Interest expense related to portfolio income. . . . . . . . . . . . . . . . . . . . .

8 Other expenses related to portfolio income (attach schedule) . . . . .

9 Other separately stated business items (attach explanation) . . . . . .

10 Small business health insurance premiums (attach explanation) . . .

11 Separately stated nonbusiness items (attach schedule) . . . . . . . . . .

12 Composite payment made on behalf of owner/shareholder . . . . . . .

13 U.S. taxes paid (attach explanation) . . . . . . . . . . . . . . . . . . . . . . . . . . .

14 Alabama exempt income (attach explanation) . . . . . . . . . . . . . . . . . . .

Transactions with Owners:

15 Property distributions to owners . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

|

|

|

|

|

|

|

Page 4 |

|

|

Federal Amount |

|

Apportionment |

|

Alabama Amount |

|

Enter on Alabama |

|

|

|

|

|

|

||||

|

|

|

|

|

||||

|

|

Factor |

|

|

Schedule |

|

||

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

|

|

Part III, Line M |

|

• |

|

|

|

|

|

|

Part III, Line S |

|

• |

|

|

|

|

|

|

Part III, Line Z |

|

• |

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

Part III, Line O |

|

• |

|

|

|

|

|

|

Part III, Line W |

|

• |

|

|

|

|

|

|

Part III, Line Q |

|

• |

|

|

|

|

|

|

Part III, Line P |

|

• |

|

|

|

|

|

|

Part III, Line R |

|

• |

|

|

|

|

|

|

Part III, Line T |

|

|

|

|

|

• |

|

|

Part III, Line Y |

|

• |

|

|

|

|

|

|

Part III, Line AA |

|

|

|

|

|

• |

|

|

Part III, Line U |

|

• |

|

|

|

|

|

|

Part III, Line V |

|

• |

|

|

|

|

|

|

Part III, Line AB |

|

• |

|

|

100% |

• |

|

|

Part III, Line X |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

•I authorize a representative of the Department of Revenue to discuss my return and attachments with my preparer.

|

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, they are |

|||||

Please |

true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

|||||

|

|

|

|

|

|

|

Sign |

|

|

|

|

|

|

Signature |

Date |

|

Daytime Telephone No. |

Social Security No. |

||

Here |

|

|||||

|

|

|

|

|

||

of Officer |

|

|

( |

) |

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

Title |

|

|

|

|

|

|

of Officer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer’s |

Telephone No. |

|

Date |

Preparer’s Social Security No. |

|

|

|

|

|

|

|

|

|

Signature |

•( |

) |

|

• |

• |

|

|

|

|

|

|

|

Paid

Preparer’s

Use Only

Firm’s Name (or yours • if

and address •

Address

E.I. No. •

ZIP Code •

CHECK LIST

HAVE THE FOLLOWING FORMS BEEN ATTACHED TO THE FORM 20S:

ALABAMA SCHEDULE

ALABAMA SCHEDULE NRA (if applicable)

FEDERAL FORM 1120S (entire form as filed with IRS)

FEDERAL FORM 1120S PROFORMA (if applicable)

FORM

Returns without Payments |

Returns with Payments |

||

|

|

|

|

MAIL TO: Alabama Department of Revenue |

MAIL TO: Alabama Department of Revenue |

||

Pass Through Entity |

Pass Through Entity |

||

PO Box 327441 |

PO Box 327444 |

||

Montgomery, AL |

Montgomery, AL |

||

ADOR

Form Specs

| Fact Name | Detail |

|---|---|

| Purpose | Alabama Form 20S is a tax return for S corporations for the tax year 2010. |

| Filing Requirement | Required by the Alabama Department of Revenue for reporting an S corporation's income, deductions, and taxes. |

| Tax Year Coverage | For the year January 1, 2010, through December 31, 2010, or other tax year beginning in 2010. |

| Sections | Includes data summary, schedule A for income/tax computation, schedule B for nonbusiness income, schedule C for apportionment factor, and more. |

| Governing Law | Governed by Alabama state laws related to S corporation taxation. |

| Mandatory Attachments | Requires attachment of Federal Form 1120S and may include Schedule K-1 for each shareholder. |

| Filing Address | Different addresses for returns with payments and without payments; specified on the form. |

Detailed Guide for Writing Alabama 20S

Embarking on the journey of completing the Alabama 20S form requires care and attention to detail. This document is vital for S Corporations registered in Alabama, as it addresses specific information regarding their operations within the fiscal year. Before you begin, ensure all relevant financial documents are accessible to facilitate the accuracy of the information you're about to provide. Below is a step-by-step guide aimed at simplifying this process for you.

- Start by entering the tax year and the exact dates covering your fiscal year at the top of the form.

- Provide the S Corporation's Federal Employer Identification Number (FEIN) and Federal Business Code Number.

- Fill in the S Corporation's official name, address, state of incorporation, nature of business, and the date the business qualified in Alabama.

- Indicate the total number of shareholders during the tax year and check the appropriate box for initial, final, or amended return.

- If the S Corporation operates in more than one state, ensure to check the corresponding box.

- Under "Data Summary," record the total federal income, deductions, and assets as shown on your federal Form 1120S.

- Input the Alabama Apportionment Factor from Schedule C, line 26 if applicable.

- Complete Schedule A by listing separately stated and nonseparately stated income or tax items, ensuring to attach any required schedules or documents for specific lines as instructed.

- For S Corporations operating both within and outside Alabama, fill in Schedule C with details about tangible property, payroll, and sales to calculate the Alabama Apportionment Factor.

- In Schedule D, input the apportionment of federal income tax based on the Alabama income from Schedule E.

- Determine and list the nonseparately stated and separately stated income allocated and apportioned to Alabama in Schedule E.

- Document any tax credits the S Corporation is eligible for in Schedule G.

- Provide detailed contact information and operations description in Schedule H.

- Accurately complete Schedule K with the distributive share items, ensuring each section is filled out completely based on the federal amounts and specific allocations to Alabama.

- Thoroughly review the form to ensure all information is correct and complete. Sign and date the form, along with the paid preparer's information if applicable.

- Attach all required documents, including any specified schedules, the entire federal Form 1120S as filed with the IRS, and Form BIT-V if you're paying by check or money order.

- Lastly, depending on whether you're including a payment with your return, mail the completed form and any attachments to the appropriate Alabama Department of Revenue address as indicated on the last page of the instructions.

Accurately completing the Alabama 20S form is essential to ensure compliance with state tax obligations and to avoid potential penalties. Taking the time to double-check each entry for accuracy will serve your business well in the long-term. Should you have any questions or require assistance, consulting with a tax professional is recommended.

Common Questions

What is the Alabama 20S form used for?

The Alabama 20S form is utilized by S corporations to file their state income tax return in Alabama. It captures details regarding the corporation's income, deductions, losses, and tax payments for the tax year specified. This form is a medium through which S Corporations report their earnings, as well as apportion and allocate income to Alabama.

Who needs to file the Alabama 20S form?

S corporations operating in Alabama are required to file the 20S form. These are entities that have elected the special tax status under Subchapter S of the Internal Revenue Code. Businesses operating in more than one state, as well as those exclusively in Alabama, should use this form, taking care to properly apportion and allocate income as per the state's regulations.

What schedules are attached to the Alabama 20S form?

Several schedules are attached to the Alabama 20S form to provide detailed information. These include Schedule A for the computation of separately and nonseparately stated income and tax, Schedule B for the allocation of nonbusiness income, Schedule C for the apportionment factor, Schedule D for apportionment of Federal Income Tax, Schedule E for the apportionment and allocation of income to Alabama, Schedule F for Alabama Accumulated Adjustments Account, Schedule G for tax credits, and Schedule K for distributive share items. Each schedule serves to break down specific areas of the corporation's financials pertinent to tax calculations and allocations in Alabama.

Are there any specific tax credits that can be claimed on the Alabama 20S form?

Yes, the Alabama 20S form Schedule G allows S corporations to claim specific tax credits. These can include the Employer Education Tax Credit and the Coal Credit among others. These credits can reduce the amount of tax owed by the corporation. It's important for corporations to review the instructions for Schedule G to understand eligibility for these credits and how they can be applied.

How does an S corporation apportion income to Alabama?

An S corporation apportions income to Alabama using the apportionment factor calculated on Schedule C of the 20S form. This involves determining the ratios of property, payroll, and sales in Alabama to the total of these factors everywhere. The sum of these ratios, divided by three, results in the Alabama apportionment factor that is applied to apportionable income, thereby calculating the income attributable to Alabama.

What are the filing requirements for an S corporation reporting changes from a previous tax year?

If an S corporation's information has changed from the previous tax year, such as its address, it needs to indicate this on the 20S form by checking the appropriate box. Moreover, if amending a previously filed return, the corporation must file an amended 20S form, ensuring to attach a copy of the Federal Form 1120S and explain the reasons for amendment. It's crucial for the corporation to keep their filing status updated and accurate, reflecting any changes in the business or its operations to ensure compliance with Alabama tax laws.

Common mistakes

Filling out the Alabama 20S form can be a daunting process for S corporations, especially considering the intricate details and the potential financial implications of mistakes. One common error involves the incorrect enumeration of total federal income and deductions. It's crucial to ensure that all income and deductions reported on the federal Form 1120S are accurately transcribed onto the Alabama 20S form. Discrepancies in these figures can lead to miscalculations of tax obligations, leading to underpayments or penalties.

Another area often mishandled is the Alabama Apportionment Factor from Schedule C, line 26. This critical value determines the portion of income considered to be generated within Alabama and, consequently, subject to state taxes. Corporations operating in multiple states must prudently calculate this figure to correctly apportion their income. Mistakes here could significantly affect the amount of state income tax owed, potentially resulting in audits or additional assessments.

Additionally, many filers overlook the relevance of accurately listing their federal employer identification number (FEIN) and the correct state of incorporation. These identifiers are not just bureaucratic details; they're essential for ensuring that the state tax department correctly attributes your return to your entity. A mismatch or typographical error can cause processing delays, misapplied payments, or filings to go unrecognized, necessitating corrections and possible penalty assessments for "unfiled" returns.

- Not attaching a copy of the federal Form 1120S, rendering the Alabama 20S return incomplete. This omission can halt the processing of the return, leading to potential penalties for late submission.

- Miscalculation or misunderstanding of the net Alabama nonseparately stated income or (loss). This figure, crucial for understanding the taxable income attributed to Alabama, is derived from combining the federal ordinary income with adjustments specific to Alabama tax law. Errors here can lead to incorrect tax liabilities being reported.

- Incorrect entries on Schedule K, pertaining to the distributive share items, particularly the separately stated items that need distinct treatment for state tax purposes. Accurate and detailed attention to this schedule ensures correct tax treatment for shareholders, potentially affecting their individual tax responsibilities.

- Failure to accurately complete SCHEDULE D and E, which are essential for apportioning federal income tax to Alabama and determining the accurate tax allocation and apportionment to Alabama. Missteps in these schedules can lead to disproportionate tax burdens.

- Neglecting to check or incorrectly checking the boxes for initial, final, amended returns, or whether the corporation operates in more than one state. This information is critical for tax processing purposes and informs the state about specific considerations for the filing.

In conclusion, when completing the Alabama 20S form, attention to detail is paramount. Through careful review and accurate reporting, S corporations can ensure compliance with state tax obligations, minimizing the risks of penalties and interest for reporting errors. It is advisable for entities, especially those with complex tax situations, to consult with professionals to ensure their filings are correct and complete.

Documents used along the form

When preparing an Alabama Form 20S, several additional documents are typically required to ensure comprehensive compliance with Alabama's tax regulations. These documents support the Form 20S by providing detailed information about the S corporation's financial activities, its shareholders, and specific deductions or credits claimed. This helps in the accurate calculation of tax liability and ensures that tax reporting is aligned with federal and state requirements. The following documents are often used along with Alabama Form 20S:

- Federal Form 1120S: This is the U.S. Income Tax Return for an S Corporation. It provides a detailed account of the corporation’s income, gains, losses, deductions, credits, and other information necessary for the state form. Since Alabama Form 20S requires inclusion of total federal income and deductions, attaching the Federal Form 1120S ensures consistency between federal and state tax records.

- Alabama Schedule K-1: This schedule is used to report the distributive share items of income, deductions, and credits to each shareholder. It ensures that each shareholder reports their correct share of the corporation's income and deductions on their individual tax returns. This schedule ultimately ties back to the information reported on the Form 20S.

- Alabama Schedule NRA: Applicable if the S Corporation has shareholders who are non-residents of Alabama. This schedule is used for calculating the amount of income that is sourced to Alabama for non-resident shareholders and is necessary for ensuring that income is properly apportioned according to state law.

- Form BIT-V: This form accompanies payment when the tax due is paid by check or money order rather than electronically. It ensures that the payment is correctly applied to the S Corporation’s tax account.

Together, these documents facilitate a thorough examination of the S Corporation's activities throughout the fiscal period. The completion and submission of these forms ensure compliance with both state and federal tax obligations, help avoid potential penalties for incomplete or inaccurate filings, and provide a clearer financial picture of the entity's operations within the state of Alabama. Each form plays an integral role in the preparation of an Alabama Form 20S, enhancing the accuracy and efficiency of tax reporting for S Corporations.

Similar forms

The Alabama 20S form is similar to the Federal Form 1120S in several aspects, primarily serving the same purpose for S corporations but at different governmental levels. Just like its federal counterpart, the Alabama 20S form is designed for S corporations to report their income, deductions, and credits to the state tax authorities. Both forms require detailed financial information about the corporation's activities during the fiscal year, including total income, deductions, and the apportionment of income among shareholders. Additionally, they both have sections dedicated to calculating tax owed or refunds due to the corporation, along with schedules for reporting specific types of income or deductions. While the Federal Form 1120S reports to the IRS and addresses federal tax obligations, the Alabama 20S targets the Alabama Department of Revenue to comply with state tax requirements. This alignment ensures that S corporations can navigate through both federal and state tax obligations with structured guidance.

Furthermore, the Alabama 20S form shares similarities with Schedule K-1 (Form 1120S), which is used at the federal level. The Schedule K-1 is essential for reporting each shareholder's share of the corporation's income, deductions, and credits. Likewise, the Alabama 20S includes a distributive share items section, which necessitates detailing each shareholder's portion of income or loss, mirroring the purpose of the federal Schedule K-1. Both documents facilitate transparent communication of individual tax responsibilities derived from corporate activities, allowing shareholders to accurately report their share of income or loss on their personal tax returns. The key difference lies in the jurisdiction: the federal Schedule K-1 pertains to IRS filings, whereas the distributive share section of the Alabama 20S form applies to state tax obligations within Alabama.

Dos and Don'ts

Filing out the Alabama 20S form for S corporations can be intricate. To aid in this process, here are several do's and don'ts that can help ensure accuracy and compliance:

- Do ensure that all information matches the records submitted to the federal IRS, particularly details like the Federal Employer Identification Number and the total federal income.

- Do correctly calculate the Alabama Apportionment Factor from Schedule C, line 26, if your corporation operates in more than one state. This is critical for determining your tax obligations to Alabama accurately.

- Do attach a copy of Form 1120S as filed with the IRS, unless you have nothing to report in this section, as the return is considered incomplete without it.

- Do accurately report all separately stated and nonseparately stated income and deductions as required on Schedule A, ensuring alignment with federal reporting to avoid discrepancies.

- Don't forget to check the appropriate boxes if it's an initial return, amended return, or if you're filing for a final return. This information guides the processing of your form.

- Don't overlook the signing and dating of the form. An unsigned form can result in delays or be considered invalid, necessitating a resubmission.

- Don't ignore the instructions for Schedules D, E, and F as they provide details on apportioning federal income tax, and apportioning and allocating income to Alabama, which are pivotal in determining your tax liability accurately.

Following these guidelines diligently will help ensure that your filing is both compliant and reflective of your corporation's financial activities within the tax year. Always refer to the latest forms and instructions from the Alabama Department of Revenue to keep up with any changes or additional requirements.

Misconceptions

There are numerous misconceptions about the Alabama Form 20S, an essential document for S corporations operating within the state. Below are seven common misunderstandings and clarifications to provide a better understanding of its requirements and implications.

- Misconception 1: The Alabama 20S form is optional for S corporations. This is incorrect. The Alabama 20S form is mandatory for all S corporations doing business in Alabama. It serves as the S corporation's annual tax return, reporting income, deductions, profits, losses, and taxes due to the state.

- Misconception 2: All income reported on the federal Form 1120S must be reported in the same way on the Alabama 20S form. While the Alabama 20S form does require information from the federal Form 1120S, adjustments may be necessary. Alabama-specific modifications can include state tax additions or deductions not required on the federal return.

- Misconception 3: The Alabama 20S form only includes income derived from Alabama. This is not accurate. The form requires the reporting of all income and deductions, including those from outside Alabama. However, it also includes sections for calculating how much of this income is subject to Alabama state tax through apportionment and allocation schedules.

- Misconception 4: When the Alabama 20S form is submitted, no other documents need to be attached. In many cases, additional documents are required. For instance, unless a copy of the federal Form 1120S is attached, the Alabama 20S return is considered incomplete. Other necessary attachments may include schedules and statements supporting the information reported on the return.

- Misconception 5: The Alabama 20S form doesn’t affect shareholder's individual state tax filings. This misconception is false. The form includes schedules, like Schedule K-1, that report each shareholder's share of income, deductions, and credits. Shareholders need this information to complete their own state tax returns.

- Misconception 6: Filing the Alabama 20S form means that S corporation shareholders don't need to file individual Alabama income tax returns. Shareholders of an S corporation must still file individual income tax returns in Alabama. The income, deductions, and credits from the S corporation flow through to the shareholders and must be reported on their personal tax returns.

- Misconception 7: The Alabama Department of Revenue provides a direct online filing option for the 20S form. As of the last update, Alabama requires certain forms to be filed electronically through approved software or via specific online platforms. However, filers should always check the current Alabama Department of Revenue guidelines, as filing options and requirements may change.

Understanding these key points can help avoid common errors and ensure compliance with Alabama's tax laws for S corporations and their shareholders.

Key takeaways

Understanding how to correctly fill out and utilize the Alabama 20S form is crucial for S corporations operating within the state. Below are four key takeaways that provide invaluable guidance through this complex process:

- Complete inclusion of Federal Forms is essential. The Alabama 20S form requires the attachment of the complete Federal Form 1120S as filed with the IRS. This requirement underscores the interconnectedness of federal and state tax reporting and ensures that revenue authorities have all the necessary data to verify state tax obligations against federally reported information.

- Meticulous reporting of nonbusiness income is necessary. As detailed in Schedule B of the form, nonbusiness income, loss, and expenses must be accurately identified and reported. This is pivotal for distinguishing between income that is subject to apportionment across various states and income that is allocated directly to Alabama - impacting the calculation of taxable income within the state.

- The role of the Alabama apportionment factor, derived from Schedule E, cannot be overstated. It represents the percentage of total income that is subject to Alabama state income tax. This factor is calculated taking into consideration the S corporation’s business activity in Alabama vis-à-vis its total business activity everywhere. This underscores the importance of precise calculation in ensuring the correct amount of income is taxed by the state.

- Adhering to the declaration and signature guidelines is the final, yet critical, step in the submission process. The form makes it clear that a declaration under penalties of perjury by an authorized officer of the S corporation is necessary for the completion and submission of the 20S form. Additionally, there’s a section for the preparer’s information, further emphasizing the importance of accountability and the accuracy of the information provided.

Each of these points highlights the critical aspects of compliance and the due diligence required when dealing with the Alabama 20S form, ensuring that S corporations accurately report and contribute their fair share of state taxes.

Check out Popular PDFs

Department of Public Safety Alabama - Guides users through the process of filing safety complaints or concerns with the appropriate authorities.

P-ebt Alabama - Verifying citizenship and immigration status is a requisite part of the application, defining eligibility for food assistance benefits.