A 3 Alabama Template

Understanding the Form A-3, Alabama’s Annual Reconciliation of Income Tax Withheld, is crucial for employers who navigate the complexities of tax filing each year. This form plays a fundamental role in reconciling the amount of Alabama income tax withheld from employees' wages with the actual tax remitted to the Alabama Department of Revenue. Specifically designed for employers who submit 25 or more W-2s, or those who have transitioned to electronic filing and payments within the fiscal year, it mandates electronic submission to streamline processing and enhance accuracy. The form’s due date is set firmly at the end of January following the tax year in question, emphasizing the need for timely compliance. Employers must accurately report monthly or quarterly withheld Alabama income taxes, depending on the amount withheld or the chosen reporting schedule, and reconcile these figures with their remitted tax amounts. The inclusion of W-2 and 1099 forms, for those applicable, with Alabama income tax withheld, is essential. Additionally, the form addresses the procedure for reporting overpayments and underpayments, providing options for refunds or future credit. It underscores the importance of accuracy and the legal obligation of employers to report and reconcile withheld income taxes, ensuring they meet their responsibilities to both their employees and the Alabama Department of Revenue.

A 3 Alabama Example

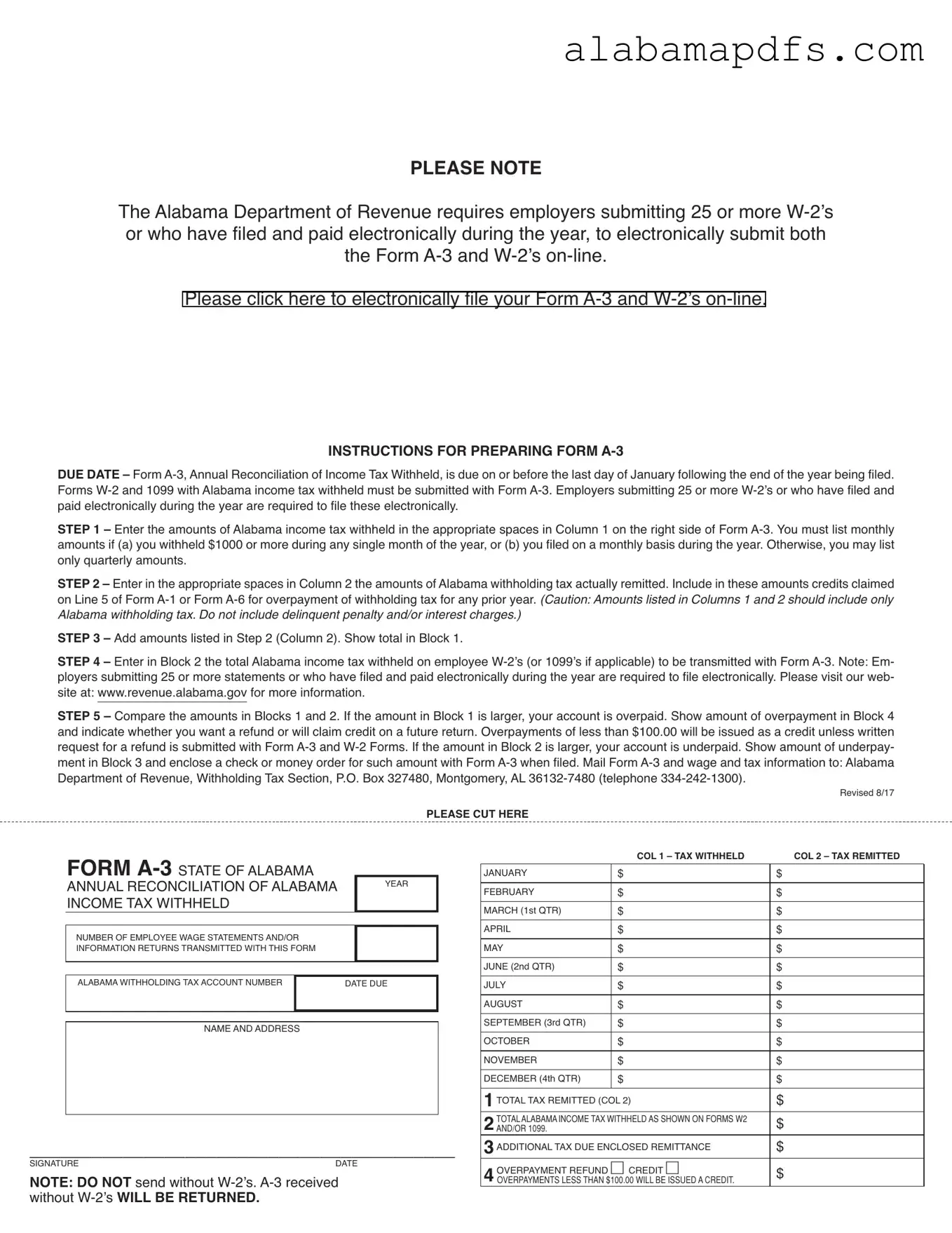

PLEASE NOTE

The Alabama Department of Revenue requires employers submitting 25 or more

Please click here to electronically file your Form

INSTRUCTIONS FOR PREPARING

STEP1 – Enter the amounts of Alabama income tax withheld in the appropriate spaces in Column 1 on the right side of Form

STEP3 – Add amounts listed in Step 2 (Column 2). Show total in Block 1.

STEP4 – Enter in Block 2 the total Alabama income tax withheld on employee

STEP5 – Compare the amounts in Blocks 1 and 2. If the amount in Block 1 is larger, your account is overpaid. Show amount of overpayment in Block 4 and indicate whether you want a refund or will claim credit on a future return. Overpayments of less than $100.00 will be issued as a credit unless written request for a refund is submitted with Form

Revised 8/17

PLEASE CUT HERE

|

|

ANNUAL RECONCILIATION OF ALABAMA |

YEAR |

|

|

INCOME TAX WITHHELD |

|

NUMBER OF EMPLOYEE WAGE STATEMENTS AND/OR

INFORMATION RETURNS TRANSMITTED WITH THIS FORM

ALABAMA WITHHOLDING TAX ACCOUNT NUMBER |

DATE DUE |

|

|

NAME AND ADDRESS

_________________________________________

SIGNATURE DATE

NOTE: DO NOT send without

without

|

COL1 – TAX WITHHELD |

COL2 – TAX REMITTED |

|

|

|

JANUARY |

$ |

$ |

|

|

|

FEBRUARY |

$ |

$ |

|

|

|

MARCH (1st QTR) |

$ |

$ |

|

|

|

APRIL |

$ |

$ |

|

|

|

MAY |

$ |

$ |

|

|

|

JUNE (2nd QTR) |

$ |

$ |

|

|

|

JULY |

$ |

$ |

|

|

|

AUGUST |

$ |

$ |

|

|

|

SEPTEMBER (3rd QTR) |

$ |

$ |

|

|

|

OCTOBER |

$ |

$ |

|

|

|

NOVEMBER |

$ |

$ |

|

|

|

DECEMBER (4th QTR) |

$ |

$ |

|

|

|

1TOTAL TAX REMITTED (COL 2) |

$ |

|

|

|

|

2AND/ORTOTAL ALABAMA1099. INCOME TAX WITHHELD AS SHOWN ON FORMS W2 |

$ |

|

3ADDITIONAL TAX DUE ENCLOSED REMITTANCE |

$ |

|

|

|

|

4OVERPAYMENT REFUND CREDIT |

$ |

|

OVERPAYMENTS LESS THAN $100.00 WILL BE ISSUED A CREDIT. |

|

|

Form Specs

| Fact | Description |

|---|---|

| Electronic Filing Requirement | Employers who submit 25 or more W-2s or have filed and paid electronically during the year must file Form A-3 and W-2s online. |

| Due Date | Form A-3 is due by the last day of January following the end of the year being reported. |

| Forms to be Submitted | Forms W-2 and 1099 with Alabama income tax withheld must be submitted with Form A-3. |

| Withholding Amounts | You must list monthly Alabama income tax withheld amounts if over $1000 was withheld during any month, or if you filed on a monthly basis. |

| Comparison of Withheld and Remitted Tax | Form A-3 requires comparing total Alabama income tax withheld on employee W-2s or 1099s against the tax actually remitted. |

| Overpayment and Underpayment | Employers can indicate overpayment for a refund or credit on future returns. If underpaid, additional tax amount must be enclosed with the form. |

| Submission Address | Completed forms should be mailed to the Alabama Department of Revenue, Withholding Tax Section, P.O. Box 327480, Montgomery, AL 36132-7480. |

Detailed Guide for Writing A 3 Alabama

Filing the A-3 Alabama Form is a crucial annual task for businesses, ensuring that their income tax withholding details are accurately consolidated and reported to the Alabama Department of Revenue. Especially pertinent for employers who have reached a certain threshold of W-2 forms or have engaged in electronic transactions throughout the fiscal year, adherence to the procedure simplifies compliance and keeps the records straight. Here's a step-by-step guide on how to fill out the form, making sure you meet all the necessary requirements without overlooking essential details.

- Identify the total amounts of Alabama income tax withheld for each month or quarter, depending on your specific situation outlined in the instructions. Fill these amounts in the corresponding spaces in Column 1 on the Form A-3. If your withholding met or exceeded $1000 in any single month, or if you filed monthly, you need to list the monthly amounts. Otherwise, quarterly listing is acceptable.

- Proceed to Column 2, where you will detail the amounts of Alabama withholding tax you actually remitted. Ensure to include any credits you've claimed for overpayment of withholding tax from previous years, as specified on Line 5 of Form A-1 or Form A-6. Keep in mind that only the amounts pertaining to Alabama withholding tax should be entered here, excluding any penalties or interest charges.

- In Block 1, add together all the amounts you've listed in Step 2 (Column 2) and write the total sum. This will provide a comprehensive total of the tax you've remitted throughout the year.

- Determine the total Alabama income tax withheld as shown on all employee W-2 forms (or 1099 forms if applicable) that you are submitting along with Form A-3. Enter this total in Block 2. Remember, electronic filing is mandatory for employers who issued 25 or more W-2 forms or have previously filed and paid electronically.

- Compare the totals in Blocks 1 and 2. If Block 1's total is larger, indicating an overpayment, record this in Block 4 and specify whether you wish to receive a refund or apply it as a credit toward future returns. Note that overpayments under $100.00 will automatically be credited, unless a refund is explicitly requested with the submission of Form A-3 and the W-2 forms. Should Block 2's total be larger, indicating an underpayment, note the amount due in Block 3. You'll need to include a check or money order for this amount when you file Form A-3.

- Finally, send the completed Form A-3 along with the wage and tax information to the Alabama Department of Revenue. The forms should be mailed to the address provided in the instructions, ensuring all relevant documents are included for processing.

By accurately following these steps, businesses can efficiently reconcile their income tax withholding obligations with the State of Alabama, maintaining compliance and ensuring their financial responsibilities are met. It's a systematic process that, when followed diligently, contributes to a smoother operational flow regarding tax submissions and record-keeping.

Common Questions

What is Form A-3 used for in Alabama?

Form A-3, known as the Annual Reconciliation of Income Tax Withheld, is a document that employers in Alabama use to report the total income tax they have withheld from their employees' wages throughout the year. This form helps reconcile the amounts withheld with the amounts actually transmitted to the Alabama Department of Revenue.

Who is required to file Form A-3?

Any employer who has withheld Alabama income tax from employees' wages must file Form A-3. Specifically, those employers submitting 25 or more W-2s or who have filed and paid electronically during the year are required to submit Form A-3 and the associated W-2s online.

When is the deadline to file Form A-3?

The due date for submitting Form A-3 is on or before the last day of January following the end of the year being filed. This means, for any given tax year, employers must file Form A-3 by January 31 of the following year.

How do I submit Form A-3 and the required W-2 forms?

Employers can submit Form A-3 and the required W-2 forms online through the Alabama Department of Revenue's website, as electronic filing is mandatory for employers who submit 25 or more W-2s or have paid electronically at any time during the tax year. For others, the forms can be mailed to the Alabama Department of Revenue, Withholding Tax Section.

What information is needed to complete Form A-3?

To fill out Form A-3, employers need to report the total Alabama income tax withheld from employees, broken down by month or quarter, depending on their total withholding amount or filing status throughout the year. Additionally, employers must reconcile these figures with the total tax amounts actually remitted to the state.

What should I do if the total tax remitted differs from the total tax withheld on W-2s?

If the total tax remitted in Column 2 of Form A-3 is more than the total tax withheld as shown on the W-2s (Block 2), this indicates an overpayment. You should report the overpaid amount in Block 4 of Form A-3 and indicate whether you want a refund or will claim a credit. Conversely, if Block 2 is larger, it means your account is underpaid. In this case, show the underpayment in Block 3 and include the appropriate payment with your filing.

Can I receive a refund for overpayment?

Yes, if your Form A-3 shows an overpayment, you can indicate on the form whether you prefer a refund or would like to apply it as a credit for future taxes. However, for overpayments less than $100.00, the amount will be issued as a credit unless a written request for a refund accompanies your submission.

Where do I mail Form A-3 if I am not submitting it online?

For those not required to file electronically, Form A-3 and all accompanying documents should be mailed to the Alabama Department of Revenue, Withholding Tax Section, P.O. Box 327480, Montgomery, AL 36132-7480.

What happens if Form A-3 is submitted without the required W-2 forms?

If Form A-3 is received by the Alabama Department of Revenue without the required W-2 forms, it will be returned to the sender. It is crucial to include all necessary documents when filing to ensure proper processing.

How can I ensure accurate reporting on Form A-3?

To ensure accurate reporting, double-check the total amounts of Alabama income tax withheld and remitted throughout the year. Make sure only Alabama withholding tax is included in your calculations—do not include penalty or interest charges. Additionally, utilizing the electronic filing system can help reduce errors commonly associated with manual entry.

Common mistakes

Completing Form A-3, the Annual Reconciliation of Income Tax Withheld, can seem straightforward, but errors can easily creep in if you're not vigilant. Understanding the common pitfalls can save time and prevent the hassle of having to re-submit the form to the Alabama Department of Revenue. Below are five missteps frequently encountered on Form A-3.

- Not Filing Electronically When Required: Employers who submit 25 or more W-2s or have filed and paid electronically during the year must submit Form A-3 and all W-2s online. This requirement is overlooked at times, leading employers to submit paper forms when they are, in fact, required to file electronically.

- Incorrect Income Tax Withholding Entries: One of the most common errors on Form A-3 is incorrect entries in the columns for tax withheld and tax remitted. It's crucial to accurately list Alabama income tax withheld monthly or quarterly in Column 1, as this is a frequent source of confusion.

- Mismatched Total Amounts: Failing to ensure that the total Alabama income tax withheld on employee W-2s matches the total amounts reported can lead to discrepancies that prompt further inquiry from the Department of Revenue. This step is especially important as it directly impacts whether an account appears overpaid or underpaid.

- Omitting Required Attachments: Mailing Form A-3 without the required W-2 forms results in the form being returned. This oversight can delay the reconciliation process and potentially lead to penalties for late submissions.

- Overlooking the Refund versus Credit Option for Overpayments: When an overpayment is identified, employers must indicate whether they prefer a refund or if the overpayment should be credited to future returns. Failing to make this selection can result in unnecessary delays and complicate financial records.

Meticulous attention to detail can significantly streamline the filing process for Form A-3. Accuracy, thoroughness, and adherence to electronic filing requirements are key to ensuring compliance and avoiding delays. Given the emphasis on electronic submissions and the critical nature of accurate and complete documentation, prioritizing precision cannot be overstated. By sidestepping these frequently made errors, employers can foster a more efficient and error-free reconciliation and reporting process.

Documents used along the form

When dealing with the complexities of payroll and withholding taxes, certain documents are integral to ensuring compliance with Alabama state tax laws. Alongside the A-3 Annual Reconciliation of Income Tax Withheld form, there are a few key documents employers might need to complete this process effectively. Understanding these forms can make the reconciliation and reporting process smoother and more efficient.

- Form W-2, Wage and Tax Statement: This critical document reports an employee's annual wages and the amount of taxes withheld from their paycheck. It's necessary for both federal and Alabama state tax purposes. The information on the W-2 is essential for employees filling out their personal tax returns and must be submitted with the Form A-3 if the employer has 25 or more W-2s or files and pays Alabama taxes electronically.

- Form 1099: This document is used for reporting income outside of wages, salaries, and tips. For Alabama employers, Form 1099 must be included with Form A-3 if there is Alabama income tax withheld from payments to individuals not treated as employees, such as independent contractors.

- Form A-1, Employer's Quarterly Return of Income Tax Withheld: This form is used by employers to report the total income taxes withheld from employees' wages each quarter. It's crucial for reconciling with the A-3 form at the end of the year to ensure all withholdings are accurately reported and remitted to the Alabama Department of Revenue.

- Form A-6, Employer's Monthly Return of Income Tax Withheld: Similar to the A-1, the A-6 form is for employers who are required to remit Alabama income tax withholdings on a monthly basis. It aids in monthly bookkeeping and becomes a vital component of the annual reconciliation process when preparing the A-3 form.

Together, these forms represent a comprehensive approach to managing and reporting employee withholdings and earnings. By accurately completing and submitting these documents, employers fulfill their obligations and contribute to the smooth operation of payroll and tax administration within Alabama.

Similar forms

The A-3 Alabama form is similar to several other tax documents used in different jurisdictions or for other purposes, but it serves a unique role in reporting state income tax withheld by employers. Understanding its similarities and differences with other forms helps in recognizing its specific application in tax preparation and compliance.

The most comparable document to the A-3 form is the Federal Form W-3, "Transmittal of Wage and Tax Statements." Both forms are designed to accompany a batch of documents (W-2s for the W-3 and W-2s or 1099s with Alabama income tax withheld for the A-3) when sent to their respective tax agencies. The A-3 form and the W-3 have a similar purpose: to reconcile the amount of income tax withheld from employees (or contractors, as applicable) with the total amount remitted to the tax authority. However, the A-3 targets state tax reconciliation for Alabama, while the W-3 addresses federal income tax withheld.

Another document akin to the A-3 Form is the Form 941, "Employer's Quarterly Federal Tax Return." This form is utilized to report federal withholdings, Social Security, and Medicare taxes on a quarterly basis. While Form 941 is a more frequent, quarterly submission, the A-3 is an annual reconciliation specific to Alabama state income tax withheld. Both forms require the employer to calculate the total tax withheld and report how much of that amount has actually been remitted. The ongoing reporting nature of Form 621 contrasts with the A-3’s year-end wrap-up, but their roles in ensuring taxes withheld from employees are fully and accurately reported to the tax authorities underline a fundamental similarity.

Dos and Don'ts

When preparing the Form A-3, Annual Reconciliation of Income Tax Withheld, for the state of Alabama, adhere to the following guidelines to ensure accuracy and compliance:

Do:- Electronically submit your Form A-3 and W-2s online if you are submitting 25 or more W-2s or have filed and paid electronically during the year.

- Ensure forms are filed by the due date, which is the last day of January following the end of the year being filed.

- Accurately enter the amounts of Alabama income tax withheld in the spaces provided on the form, differentiating between monthly and quarterly amounts as required.

- Include with your Form A-3 all Forms W-2 and 1099 that report Alabama income tax withheld.

- Reconcile the total tax remitted with the total tax withheld as shown on W-2 or 1099 forms and accurately report any overpayment or underpayment.

- Mix Alabama withholding tax amounts with delinquent penalty and/or interest charges on the form. Keep the calculation of taxes distinct from any penalties or interests.

- Delay the submission beyond the deadline to avoid penalties and interest for late filing.

- Forget to sign and date the Form A-3. An unsigned form may result in processing delays.

- Mail the Form A-3 without including the W-2s, as forms received without W-2s will be returned, causing unnecessary delays.

- Ignore the requirement to file electronically if you meet the conditions, such as submitting 25 or more W-2’s or having filed and paid electronically during the year. Always check for the latest electronic filing procedures on the Alabama Department of Revenue website.

Misconceptions

Understanding the Form A-3 in Alabama is critical for employers, but misconceptions can lead to errors in compliance. Here we'll clarify some common misunderstandings and ensure you're on the right track.

Electronic filing is optional for all employers: This is incorrect. The Alabama Department of Revenue mandates that employers who submit 25 or more W-2 forms or have paid electronically during the year must file their Form A-3 and W-2 forms online. This requirement helps streamline the process and ensures accuracy and security.

Form A-3 is only for reconciling employee income tax: While Form A-3 is indeed used for the annual reconciliation of income tax withheld from employees, it also applies to 1099 forms with Alabama income tax withheld. It encompasses a broader scope than some might think, including both employee and non-employee compensation.

Penalties and interest can be included in the withholding tax remitted: This is a crucial point of confusion. When completing Form A-3, the amounts entered for taxes withheld and remitted should not include any penalties or interest charges. These figures should strictly represent the Alabama income tax withheld.

Any amount of overpayment automatically leads to a refund: Overpayments do indeed indicate that the employer has withheld more than what was due, but refunds for amounts less than $100 are not automatically issued; they are credited to the employer's account, unless a specific request for a refund is submitted with the form.

Only yearly totals are required for reporting: Employers must provide monthly withholding amounts if they withheld $1,000 or more during any month or if they filed on a monthly basis, rather than only the yearly total. This detail is essential for a comprehensive understanding of an employer’s withholding obligations and compliance.

Physical mailing is the only submission method: While the form and accompanying documents can be mailed to the Department of Revenue, employers required to file electronically because they submit 25 or more W-2 forms or have previously filed and paid electronically during the tax year must do so online. This clarification is vital for ensuring that submissions are made through the correct channels.

Grasping these nuances of Form A-3 can prevent errors and ensure timely compliance with Alabama's tax regulations. Whether you are filing for the first time or have done it before, staying informed about these aspects will help avoid pitfalls and streamline the reconciliation process.

Key takeaways

Filing the Form A-3 in Alabama is an essential process for employers to reconcile their income tax withholding for the year. Understanding the key takeaways of this form can streamline the process and ensure compliance with the Alabama Department of Revenue's requirements.

- The Form A-3 is due on or before the last day of January following the end of the taxable year.

- Employers who submit 25 or more W-2s, or those who have paid electronically during the year, are required to file Form A-3 and the W-2s electronically.

- When preparing Form A-3, accurately enter the amounts of Alabama income tax withheld in the spaces provided on the form. Monthly amounts should be listed if you withheld $1000 or more in any single month of the year, or if you filed on a monthly basis.

- It's crucial to include the correct amounts of Alabama withholding tax remitted. This includes any credits claimed for overpayment of withholding tax from previous years, but it does not include penalty and interest charges.

- The total tax remitted, shown in Column 2 of the form, should be summed up and recorded in Block 1.

- In Block 2, enter the total Alabama income tax withheld on employee W-2s (or 1099s, if applicable) that will be submitted alongside Form A-3.

- Comparing the totals in Blocks 1 and 2 helps identify if there is an overpayment (to be noted in Block 4) or an underpayment (to be indicated in Block 3) in your account. For overpayments less than $100.00, a credit is issued unless a refund request is submitted.

- If there's an underpayment, include a check or money order for the owed amount when filing Form A-3.

- All documentation, including the Form A-3 and wage and tax information, should be mailed to the Alabama Department of Revenue, Withholding Tax Section, at the provided address.

By keeping these key points in mind, employers can ensure that they fulfill their obligations accurately and on time, thereby avoiding potential penalties or issues with the Alabama Department of Revenue.

Check out Popular PDFs

Alabama Mvt 41 1 - The form is essential for documenting and processing salvage titles for vehicles in the state of Alabama.

Adult Adoption in Alabama - Structured as a three-page comprehensive document to cover all aspects of adult adoption consent thoroughly.

Catastrophe Savings Account Alabama - It offers a protective measure for Alabama residents wishing to file taxes via paper due to the electronic mandate.